The latest release of Statistics Canada’s Survey of Earnings, Payroll, and Hours (SEPH) for September gives us another opportunity to gauge how Canada’s labour market is faring. Most of the data isn’t great: employment across Canada fell by 57,400 jobs in September, accompanied by a small increase in the number of job vacancies, to 528,000. This brought the overall job vacancy rate up to 3.0%.

Against that backdrop, it’s notable that average weekly earnings increased to $1,280 in September—up a robust 5.2% from one year ago. This sounds great for workers—especially in light of what is moderating consumer price inflation (which fell to 1.6% in September before rising to 2.0% in October ), which has in turn yielded a strong boost to real wages after a couple of years of decline due to high inflation.

But with the job vacancy rate having fallen back to pre-pandemic levels from all-time, post-pandemic highs, and an unemployment rate that has been rising for the better part of two years (currently it sits at 6.8%), are earnings really increasing that quickly, or is something else going on? One possibility as to what “something else” might be is what we call the “composition effect”.

The composition effect refers to how changes in the distribution of characteristics within a group can affect the overall measures of a group, even if the individuals within a group are unchanged. For example, imagine a scenario where you’ve been spending more on groceries—but you’re not buying more groceries—and so you (logically) think that groceries have become more expensive. They may have, but what may have instead happened is you went from buying regular fruits and vegetables to buying organic ones, or from buying generic brands to name brands, and so your grocery bill went up even though the prices of individual groceries was unchanged.

With this example in mind, and using data from the latest SEPH, we can attempt to rule out whether or not a composition effect is in play geographically or sectorally (or both) as it relates to rising wages in Canada.

Is Growth in High-Wage Provinces Driving up Average Earnings?

First looking geographically, average weekly earnings differ substantially province-to-province (and differ even more in the Territories, although their payroll employment levels are so much less that they don’t materially affect national averages). The three provinces with the highest average wages are, in order, Alberta, Ontario, and British Columbia. Those three provinces actually saw the bulk of the job losses between August and September, and added less than their share of payroll employment over the course of the last year. To wit, these three provinces account for 65% of the country’s employment (11.5 million), but only added 58% of the net growth in jobs last year (50,000).

When we measure the contribution of the changing provincial distribution of jobs to wage growth over the past year, we find that less than 1% of overall wage growth (0.2% to be exact) can be attributed to this, while almost all of it is from increasing average earnings across the provinces (99.8% of total wage growth). So we can rule out the idea that increasing wages in Canada are simply due to higher-wage provinces growing their employment bases to a greater (proportional) extent than lower-wage ones.

Is Growth in High-Wage Sectors Driving up Average Earnings?

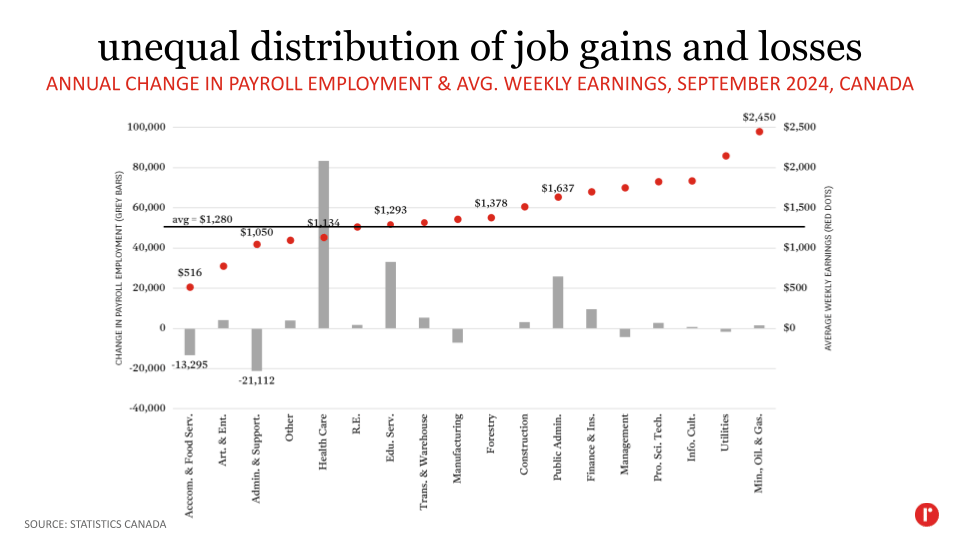

When we consider changing sectoral employment, it’s clear that both job gains and losses over the past 12 months were concentrated in just a handful of sectors. In particular, net employment growth in Canada was driven by health care (+83,415 jobs), educational services (+33,031), and public administration (+25,807), representing the 14th-, 12th-, and 7th-highest average weekly earnings among 18 sectors, respectively.

On the other hand, the bulk of the employment losses were in administrative and support (-21,112) and accommodation and food services (-13,295), which have the 3rd-lowest and lowest average weekly earnings, respectively. In other words, the data show that job losses over the past year have been concentrated in some of the lowest-earning sectors, while employment additions have been in higher-earning sectors. It’s easy to see how this dynamic could drive up overall average wage growth, even if wages didn’t necessarily increase within each individual sector.

Having said that, the changing sectoral composition of jobs in Canada over the past year only accounts for a small proportion of the overall increase in wages (2.2%), while within-sector increase in average earnings account for the vast majority of the growth (97.6%; a tiny sliver represents the synergy of the two, at 0.2%). In a nutshell, then, the data point to the sectoral composition effect being relatively weak as an explainer of overall wage growth.

So can we entirely rule out the impact of the composition effect on rising wages? Not necessarily. Indeed, there is the possibility that the composition effect is at play at an occupational level—that job losses in lower-wage occupations and gains in higher-wage occupations within each sector are driving overall wage growth. An example of this within health care might be an increase in the number of surgeons and physiotherapists alongside fewer hospital cafeteria workers and admin staff. Alas, the SEPH does not allow us to peer this granularly into the data.

So where does this leave us? Well, what we do have is a clearer picture of some of the features of our job landscape that are not driving average weekly earnings increases in this country. And come January, when new occupational data is released by Statistics Canada, we’ll see if the picture becomes even clearer.