Another month, another anemic set of retail spending data, and another piece of evidence that the Bank of Canada should cut its trend-setting interest rate at its upcoming June 5th meeting.

Across Canada, seasonally-adjusted retail spending—think spending on cars, cheese and nuts, gardening equipment, hockey tickets, those sorts of things—fell by 0.2% in March, to $66.4 billion (down from $66.5 billion in February, a month with only 29 days). The sectors registering the biggest declines were furniture & electronics (-1.6%), clothing & jewelry (-1.6%), and sporting goods (-1.5%), while spending on building and gardening equipment (+1.3%) and on motor vehicles and parts (+1.0%) rose.

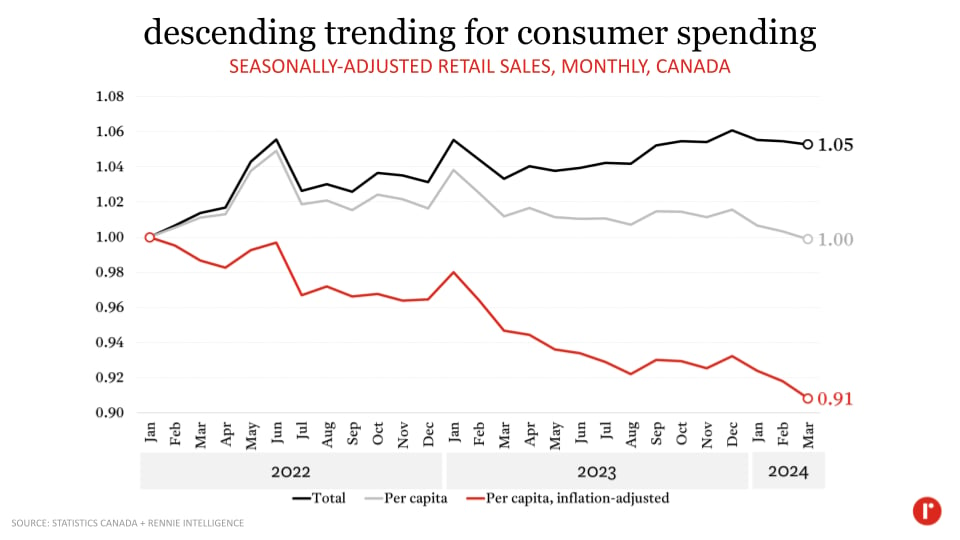

Setting aside the noise in the sectoral patterns of spending changes, the signal in all of this data lies in the longer-term trend in total retail spending—and more importantly, spending on a per-person basis.

Since January 2022—a date not chosen mainly because it’s a) the beginning of a year and b) it precedes by a few months the beginning of the Bank of Canada’s rate-hiking program—total monthly retail spending in Canada has risen by 5%, from $63.1 billion to the above-noted $66.4 billion.

On the one hand, it’s easy to look at this without becoming immediately concerned about the health of our economy (hey, 5% growth isn’t no growth). But on the other hand, consider that monthly retail spending actually grew by 5.5% in 2022, didn’t grow at all in 2023 (ok, it rose by 0.004%), and contracted by 0.25% in Q1 2024. That trend is going in the wrong direction.

Furthermore, and as we’ve noted previously, one would expect spending to increase as a natural consequence of population growth (and vice versa); ergo, let’s adjust the spending data so we can look at it on a per-capita basis. When we do this, we see that spending in March 2024 matched that of January 2022—i.e. It didn’t grow. Furthermore, per-capita spending over the past 12 months has actually fallen by 1.3%.

Now that the knife has been stuck in, we can really twist it by adjusting the per-capita spending data for inflation to get a sense for how “real” spending has changed. This generates what is by far the biggest indictment of our recent economic performance (at least as far as consumer spending is concerned), with inflation-adjusted per-capita retail spending down 9% in March 2024 from its January 2022 level; over the past year, it’s down 4.1%.

None of this is overly surprising given the once-in-a-generation escalation in interest rates that we’ve seen—which have served to disincentive leveraging and spending in favour of saving, while homeowners are devoting more of their incomes to servicing existing mortgages—but it does provide yet more fresh evidence that the time is now for our central bank to begin lowering interest rates.