It’s a consensus view among economists and analysts that import tariffs raise prices for consumers. That assessment is informed not just by theory but by recent history.

In early 2022, as demand surged for goods like furniture, food, and other household staples, it ran into a wall of pandemic-related closures at ports and warehouses. With a limited number of shipping vessels available, countries began competing for access to them. Shipping costs soared, and businesses, rather than absorbing those costs, passed them on to consumers. In part due to this (among other factors), the result was the highest inflation in over four decades.

The current tariff regime in the United States is expected to operate in much the same way—only rather than costs rising over the course of a trans-Pacific journey, they now rise the moment goods reach the port. The pressure on margins is similar, and in time, those costs tend to find their way to the consumer.

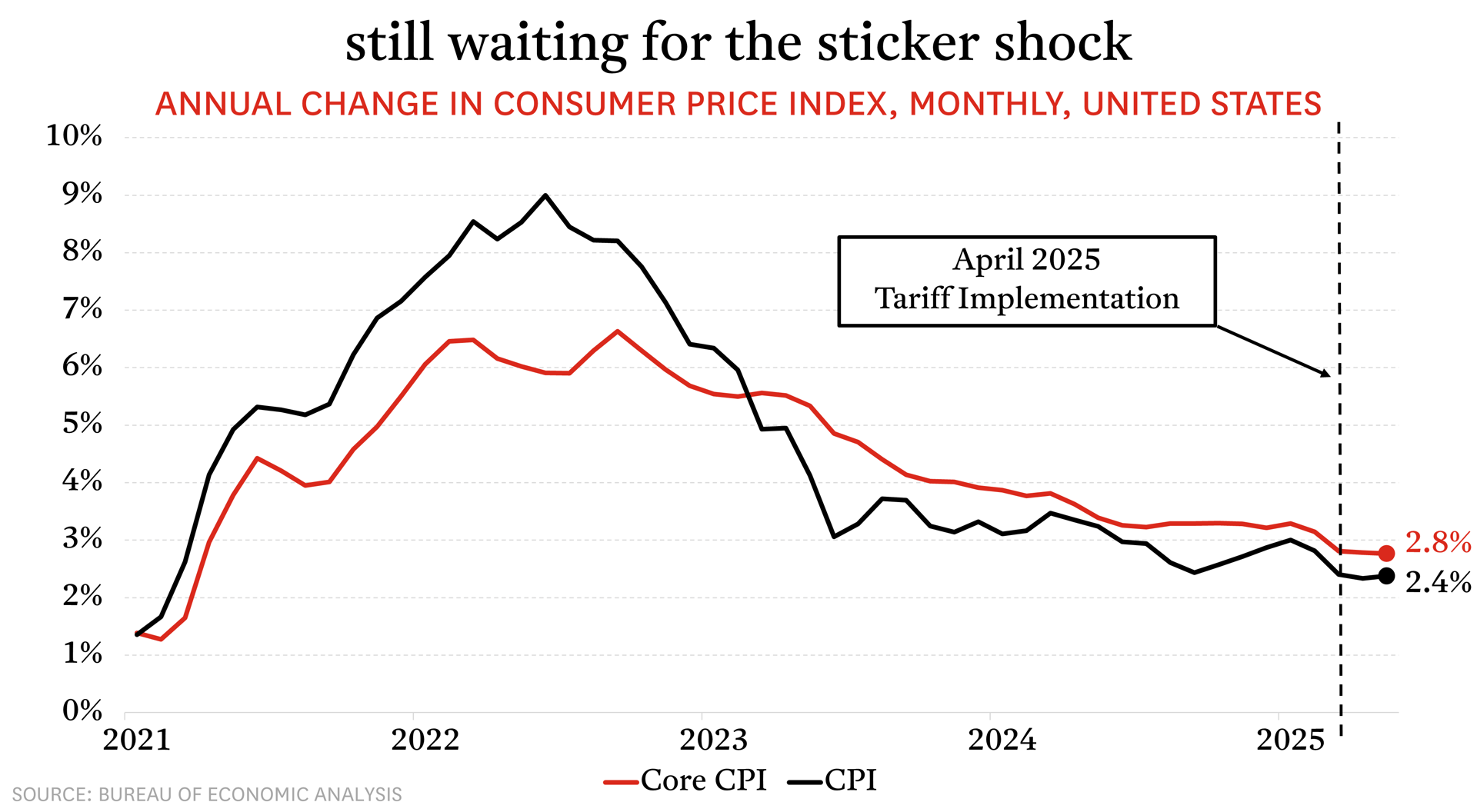

So far, though, we haven’t seen this play out. The latest reading of the Consumer Price Index, which tracks changes in the cost of consumer goods and services, came in below expectations in May. Prices rose 2.4% year-over-year, which was only slightly higher than the 2.3% increase in April—which in turn was the smallest annual gain since February 2021. Core CPI, which strips out food and energy and is seen as a clearer read on underlying inflationary trends, came in at 2.9%, also up only modestly from April’s 2.8% reading.

These are not the kind of numbers most expected, especially given the scope of the tariffs. The Treasury Department brought in $22 billion in customs duties in May —over three times the $7 billion monthly average seen over the six months leading up to the tariff implementation.

If businesses are paying more at the border, why aren’t consumers seeing it in the data? The answer isn’t straightforward, but we offer the three following observations.

1. Services Inflation Has Eased Considerably and is Bringing the Overall Print Down.

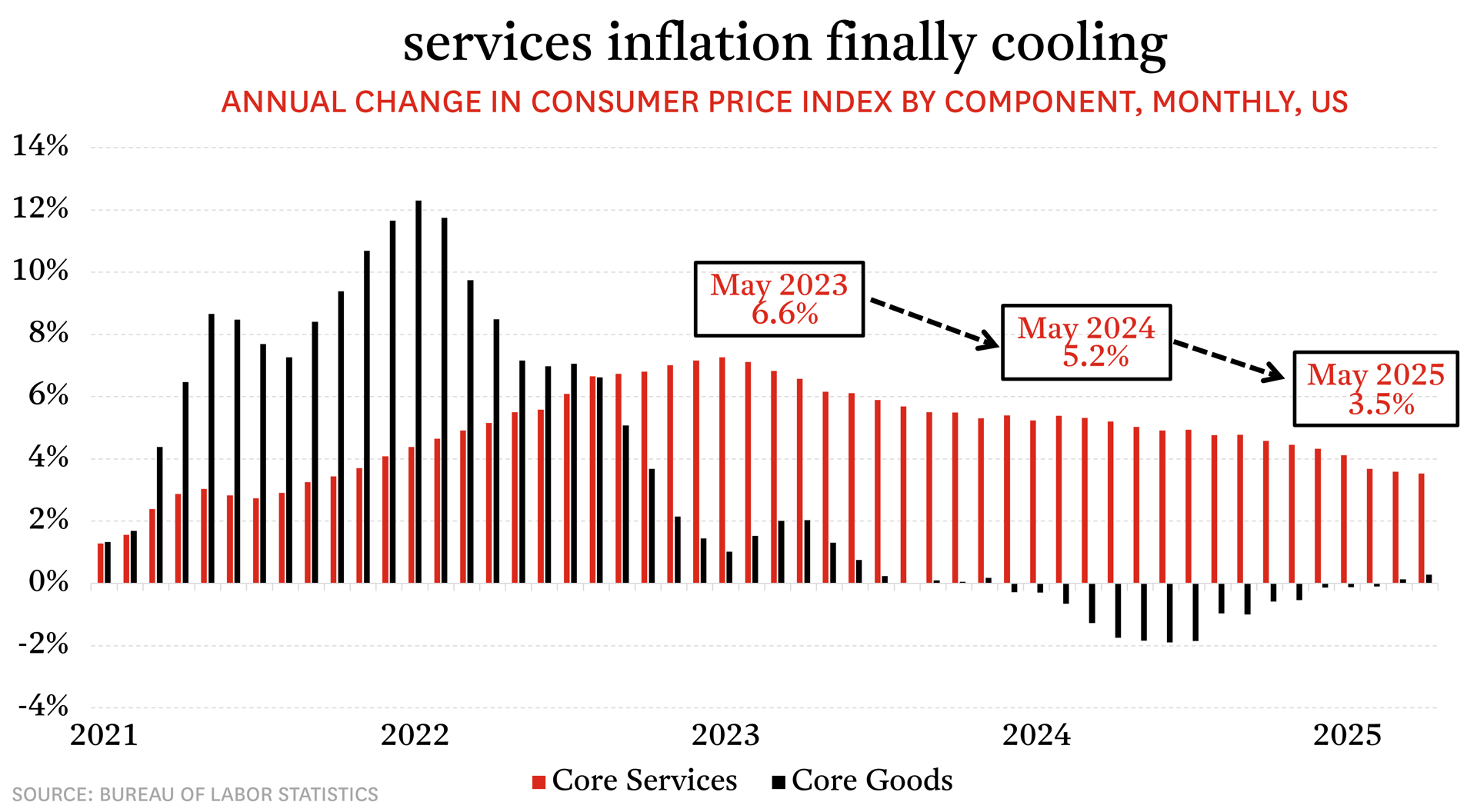

Increases to services costs, which include things like housing, insurance, and medical care, have been the major contributor to inflation since 2023. Services are naturally slow to cool, but they are indeed cooling. Near the peak in May 2023, annual services inflation was at 6.6% and, last month, it had cooled to 3.5%, which is helping to bring down the overall inflation reading.

2. Businesses Frontloaded Supplies Ahead of Tariffs, Which May Mitigate Effects.

The federal administration began issuing tariff threats in December 2024, but they were not implemented until early April. In the intervening three months, imports were elevated as businesses brought in extra goods ahead of time, in anticipation of the tariff rollout.

Given the unpredictability of tariff policy so far, it seems that businesses are first working through inventories purchased at this lower cost basis. Many firms may be holding off on raising prices until they must, in the hope that the tariffs prove short-lived.

3. Consumers May Not Be Willing to Accept Higher Prices, and Businesses Are Sensitive to This.

Inflation has been elevated for over three years, and the aggregate effect on prices is considerable. Consumers may be reaching a point where further price increases will not be tolerated, leading them to seek more economical alternatives or pull back on spending altogether.

The job market has held firm thus far, but there are some early signs of consumer pullback, such as airline prices falling (down 7% year-over-year in May) amid weaker demand.

We offer these considerations with the view that tariff-driven inflation remains a question of when, not if. It is likely that inflation will be elevated through the summer. While recent data shows a softer reading, the combination of frontloaded inventories, easing services inflation, and businesses strategically postponing price increases are likely only delaying the full impact.