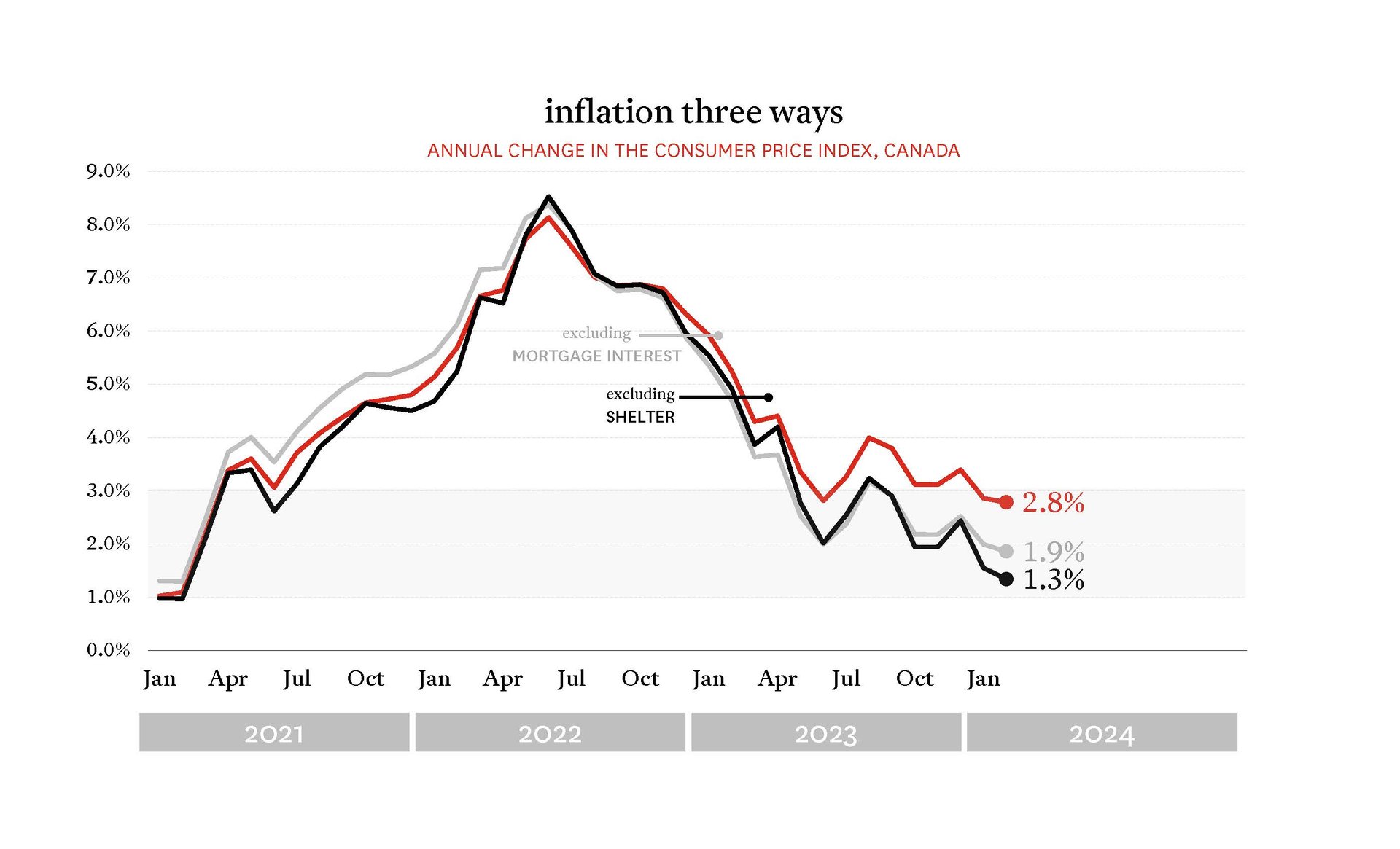

With another release of Consumer Price Index data from Statistics Canada bringing another decrease in inflation (to 2.8% in February), all eyes turn back to the Bank of Canada ahead of its next interest rate announcement. Not only has headline inflation been back inside the Bank’s target range of 1-3% for two consecutive months, but when you strip out the mortgage interest component of the CPI (which is running hot as a direct result of the Bank’s restrictive monetary policy) the rest of the CPI is actually below the 2% target.

Additionally, economic growth has been flat (GDP grew 0.25% in Q4 2023) and the labour market has been softening (unemployment rate rising to 5.8%) leading to the question of the day: when will the Bank start to cut its policy rate?

Well, to answer that question we need to consider the language from the most recent announcement on March 8th. The Bank noted “Underlying inflationary pressures persist: year-over-year and three-month measures of core inflation are in the 3% to 3.5% range, and the share of CPI components growing above 3% declined but is still above the historical average.” Additionally they said “Governing Council wants to see further and sustained easing in core inflation and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour.”

So let’s check in on the Bank’s preferred measures of core inflation, CPI trim and CPI median. Both measures declined in February to 3.2% and 3.1% respectively. Both are still outside 3% on a year-over-year basis, but trended lower last month while the three-month measures for both declined to below 3% (to 2.3% for CPI trim and 2.1% for CPI median)--a clear sign that underlying price pressures have weakened. Further, the share of components growing above 3% declined again in February, from 45% down to 40%. This is progress to be sure, and points to an interest rate cut soon, though is not definitive on its own.

As it stands now, the inflation picture is such that an interest rate cut in April is still a possibility, (and was our prediction to start the year). The first cut coming no later than June looks likely, though, with plenty more data still to come.