Resale and pre-sale markets offer buyers two very different ways to purchase residential real estate. The former is what probably comes to mind first when most people think about the housing market: existing homes that can be seen, touched, and experienced prior to purchase. These homes are move-in ready and require a down payment and financing up front. Pre-sale, on the other hand, is more like a futures market: it’s securing an option now to buy a home at some later date. Delivery of the home may not be for several years, and buyers can get a foothold in the market with smaller, staggered deposits while also delaying the need to secure a mortgage until the home is ready to be lived in.

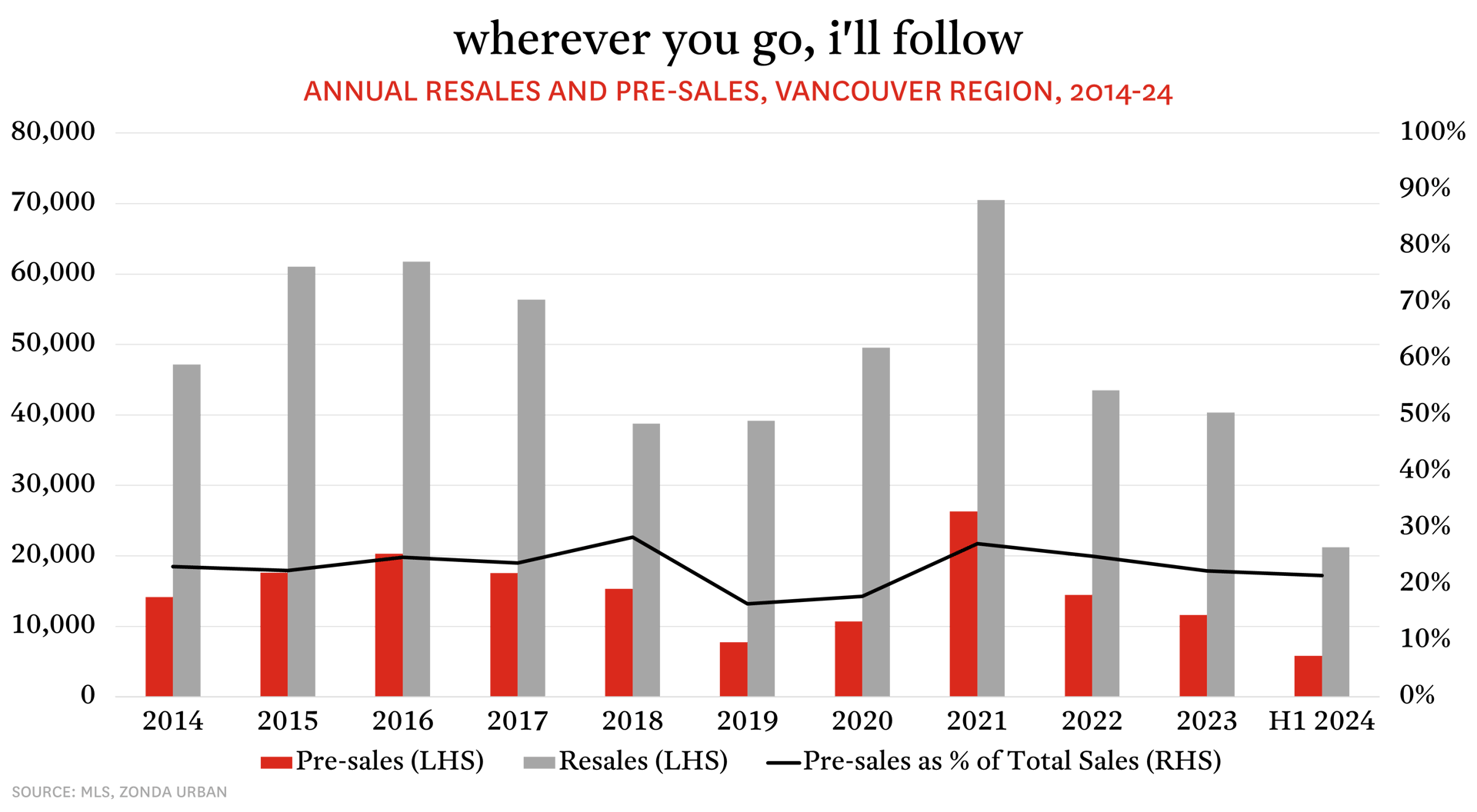

Despite these differences (and many others), resale and pre-sale activity are very strongly correlated (a sales correlation coefficient of 0.89 for the math aficionados). In fact, resale market conditions often directly influence pre-sale purchase decisions. For example, in periods of rising home prices, pre-sale activity often ramps up with buyers eager to secure their future home at today’s prices. Alternatively, in periods of elevated resale inventory, buyers may be less eager to purchase a pre-sale home with so many more options to consider. As such, activity in the two markets tends to ebb and flow with one another. In the Vancouver Region, pre-sales as a percentage of total home sales (i.e., resales plus pre-sales) have remained pretty consistent each year over the past decade, with an overall annual average of 23%.

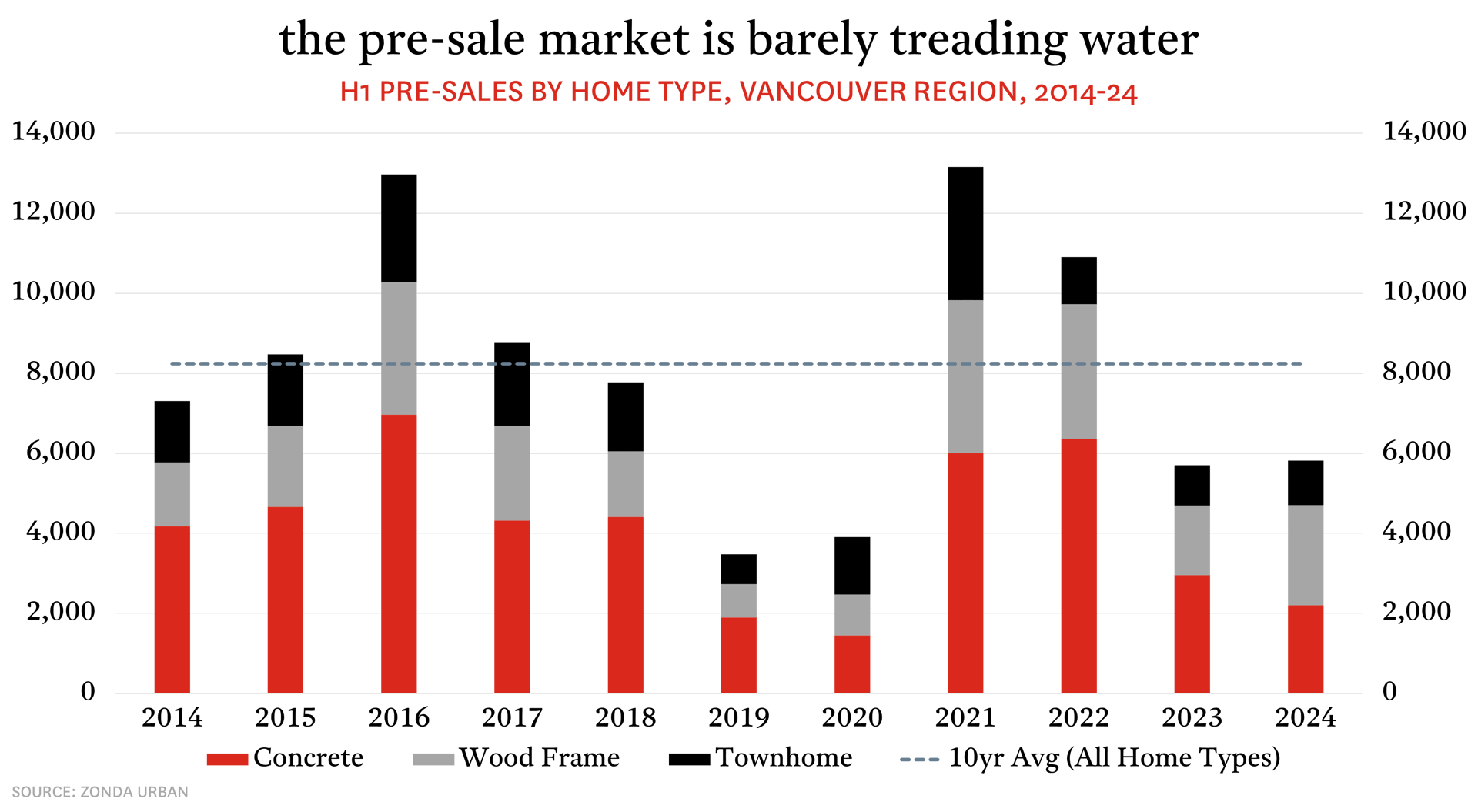

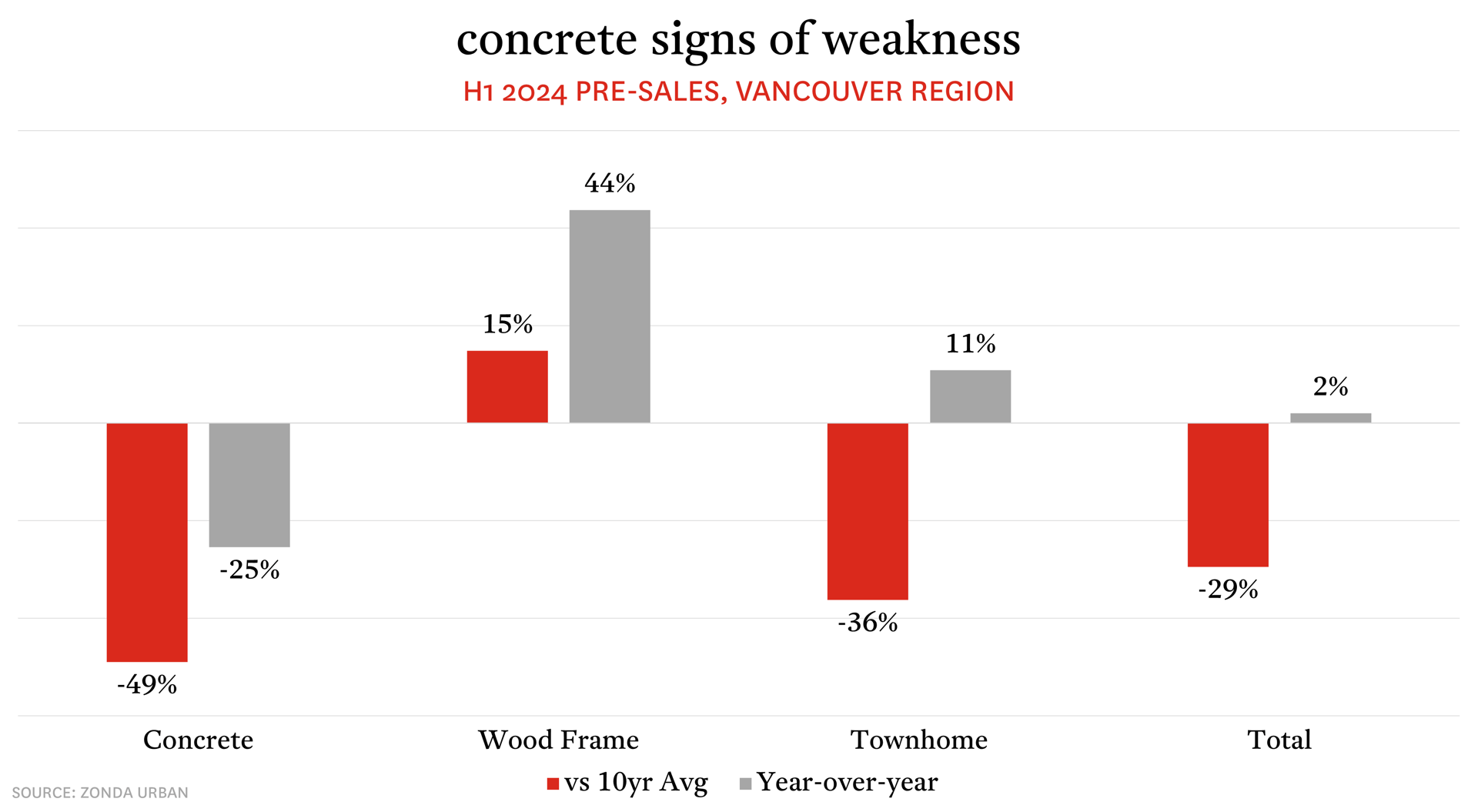

The chill blowing through Vancouver’s resale market in the first half of this year (H1 2024) has also kept activity pretty cool in the pre-sale market. Pre-sale transactions totalled 5,814 in H1 2024, 29% below their prior 10-year H1 average (versus a 22% deficit for the resale market). Slumping demand for concrete homes has especially weighed down pre-sale activity, with H1’s 2,202 sales down 25% year-over-year and 49% below the prior 10-year H1 average. Concrete homes accounted for just 38% of total pre-sales from January through June versus a little more than half in a typical year.

In contrast, wood frame pre-sales have been exceptionally strong so far in 2024, offsetting much of the weakness in the concrete space. In fact, for the first time in 11 years, wood frame pre-sales actually surpassed those of concrete with 2,498 transactions in H1 2024. This was 15% above the prior 10-year H1 average and up 44% year-over-year, helping buoy the overall pre-sale market to a small 2% increase in sales compared to the first half of 2023. As it turns out, there are a few reasons that might explain said strength for wood frame homes and the corresponding weakness in the concrete space.

No Home for Investors

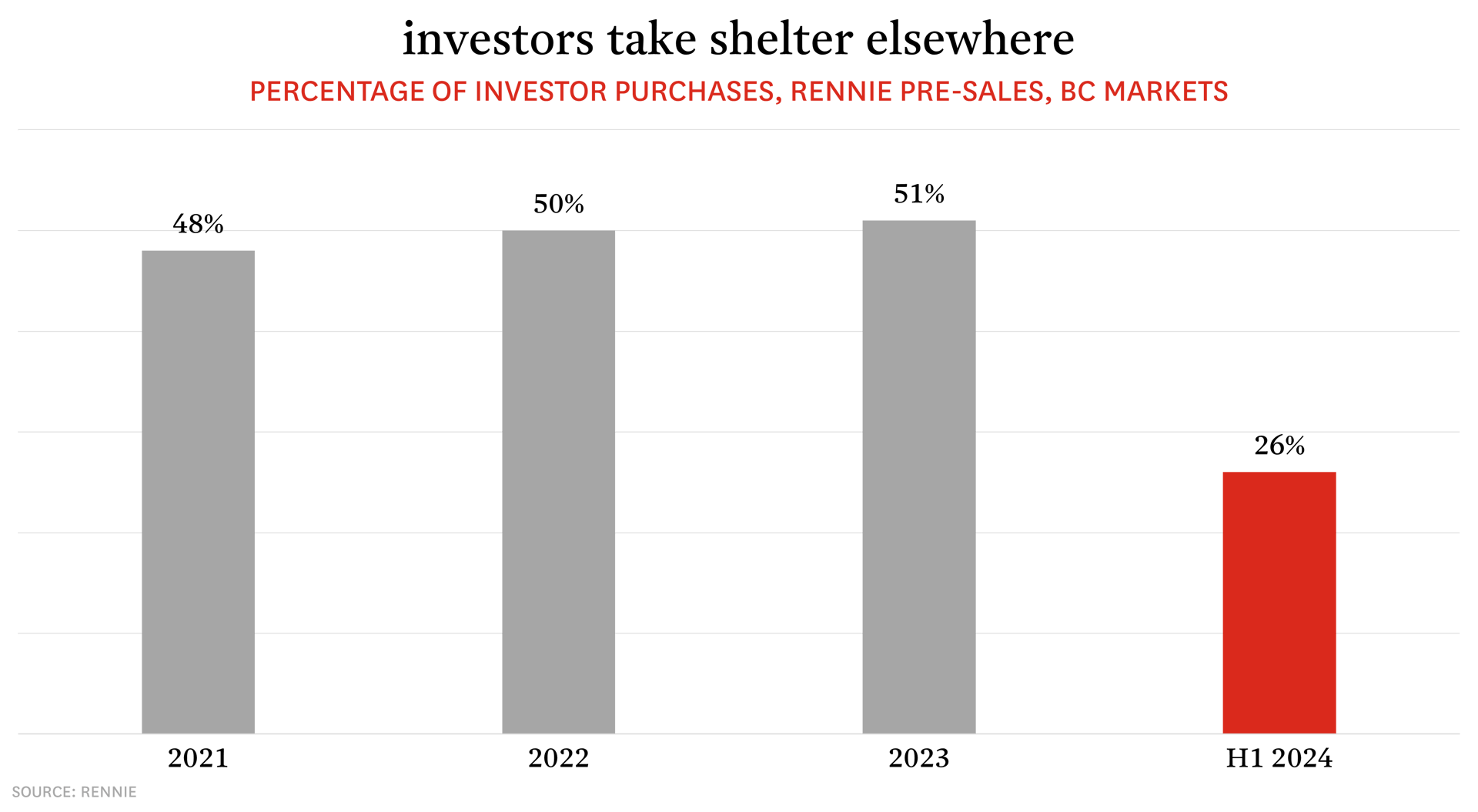

One factor contributing to more depressed concrete pre-sales and to slower activity more broadly has been a noticeable absence of investors (i.e., those purchasing homes for the purpose of renting the units to tenants). Data from thousands of pre-sale transactions at rennie shows that, as a share of total pre-sales, investor purchases fell to 26% in H1 2024 from around 50% over the prior three years. Sustained high interest rates, challenging economic conditions, and a flurry of new government policies with negative implications for investors (including increases to the capital gains inclusion rate, restrictions on short-term rentals, and changes to the Residential Tenancy Act, to name a few) have together pushed many investors to the sidelines. Contrary to mainstream narratives, fewer investors in the pre-sale market won’t free up more housing for purchase by everyday residents; instead, their absence has significant negative implications for future housing supply in the Vancouver Region, for a couple of reasons.

The first relates to the region’s long-term rental housing market. Data from the Canada Mortgage and Housing Corporation (CMHC) shows that almost 94,000 condos were used as rental housing in Metro Vancouver in 2023 versus a stock of almost 124,000 purpose-built rental units. In other words, investor-owned condos accounted for about 43% of the region’s total rental housing (excluding basement suites and other secondary market rentals). When we look at the condo market specifically (and ignore purpose-built rental units), just under a third of all condos were investor-owned rentals (31.8%). Clearly, investors make up a significant share of the region’s condo market and are key to delivering much-needed rental housing.

Having said this, to have condos available for rent in the first place requires that the buildings with condos in them be built, and the role investors play in getting homes built is arguably more important than their role in directly delivering rental housing. That is because today’s pre-sales are tomorrow’s housing starts. In the Vancouver Region, pre-sales are a key mechanism used by developers to secure construction financing, with lenders typically requiring that 60-70% of the homes (or floor space by revenue) in a project be pre-sold before a financing commitment is made.

With such a significant share of pre-sale demand (i.e., investors) now on the sidelines, it will be more challenging for developers to reach their pre-sale thresholds, to secure financing, and to ultimately build more housing. This at a time when housing unaffordability (both rented and owned) has reached crisis levels due to a severe shortage of housing supply and years of insufficient housing construction. Indeed, based on the current pace of construction CMHC estimates that British Columbia will have a shortfall of 610,000 homes in 2030 from levels needed to restore housing affordability. The majority of the province’s housing stock (and that shortfall) are in the Vancouver Region.

In the Red(Ma)

The challenging investor climate and slumping pre-sale activity has put increased attention on British Columbia’s Real Estate Development Marketing Act (REDMA), a law enacted in 2004 to regulate the marketing and sale of multi-unit real estate developments in the province. While an important tool to protect consumers and reduce the risk of bringing new housing to market, it is increasingly seen as restrictive to the delivery of new housing.

One of the key requirements of REDMA at odds with the development industry is the “early marketing period”. Under the Act, developers have just 12 months from the time that they file initial disclosure (i.e., a document containing all material facts about the development being marketed) before they must secure a financing commitment or obtain a building permit. If either of these requirements are unmet, buyers have the opportunity to take back their deposit and walk away from their pre-sale contract. Against the backdrop of an exodus of investors from the pre-sale market, reaching the 60-70% pre-sale threshold has become increasingly challenging. Requiring that threshold be met in 12 months is detached from the reality of current market conditions.

Beyond that, REDMA’s 12-month early marketing period is especially restrictive for large condo projects, the housing type most demanded by investors and most capable of bringing new housing to the region at scale. Irrespective of the current economic and investment climate, the sheer size, complexity, and cost of today’s concrete towers relative to even a decade ago is enough to justify revisiting the duration of the early marketing period.

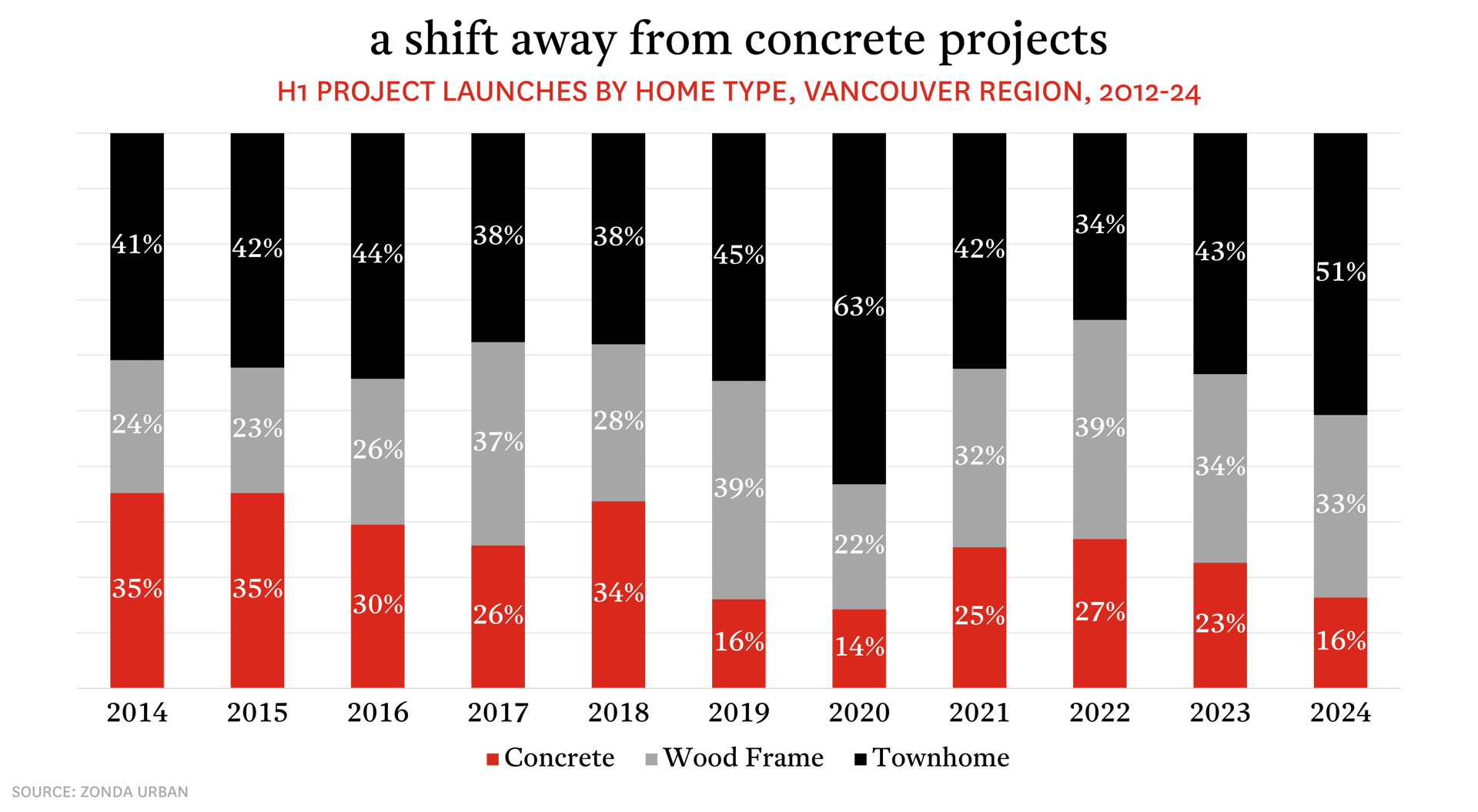

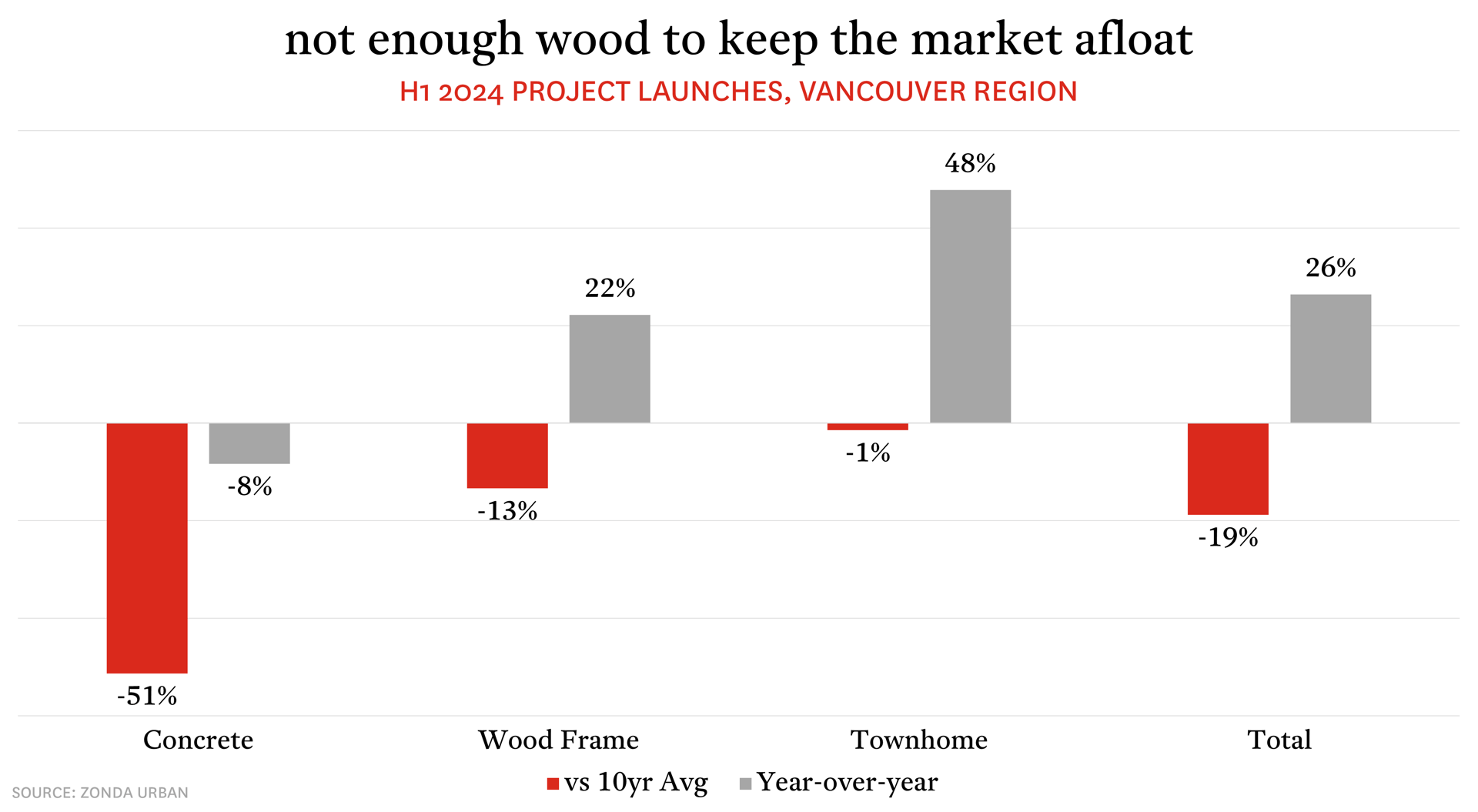

The data shows as much with the proportion of concrete project launches declining throughout the past decade. Concrete projects accounted for just 16% of the 67 total launches in H1 2024 (equivalent to 11 concrete launches), which was down 8% year-over-year and 51% below the prior 10-year H1 average (of 23 launches). Though total launches were up 26% year-over-year, this was entirely driven by a 48% year-over-year increase in townhome launches and a 22% jump in wood frame launches—smaller projects that generally offer buyers lower price points and are thus easier for developers to sell within the 12-month early marketing period. Still, total launches in H1 2024 were 19% below the prior 10-year H1 average (of 83 launches).

Unlocking the Pre-Sale Market to Deliver More Housing

Activity in the Vancouver Region’s resale and pre-sale markets has been rather subdued through the first half of 2024, with a suite of challenging economic conditions limiting buyer demand. In addition to that, an unfriendly investor climate and REDMA’s restrictive early marketing period have further challenged the development industry’s ability to launch and pre-sell homes (especially concrete). Many developers have projects that they are eager to launch, but can’t justify doing so with so much uncertainty and just 12 months to reach their pre-sale thresholds.

As market conditions begin to improve—with further declines in interest rates expected through the latter half of 2024 and through 2025—there is potential for the fall resale market to be busier than the spring and for sales activity in the second half of the year to surpass that of the first half. By extension, a re-activation of the resale market would support activity in the pre-sale market, giving developers greater confidence to launch idle projects and providing would-be buyers with more housing options. Whatever the short-term future may hold, however, governments would be wise to revisit some of the restrictive policies currently preventing the pre-sale market from being a more effective mechanism for the delivery of new, and much-needed, housing.