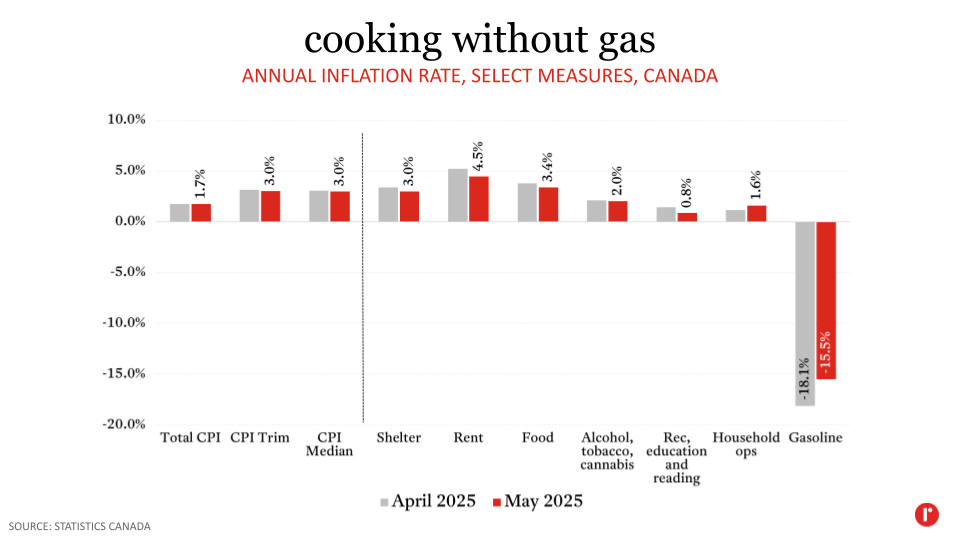

Today’s release of Consumer Price Index (CPI) data from Statistics Canada revealed no change in headline inflation in May versus April, at 1.7%. The removal of the consumer carbon tax in April has pulled the overall rate of inflation lower in each of the past two months—as it will until next April owing to the fact that inflation is calculated on a year-over-year basis. That said, the annual change in gasoline prices was smaller in May (-15.5%) than in April (-18.1%), and price growth slowed in other segments of the CPI.

Shelter inflation, which accounts for almost one-third of the CPI, slowed further in May and is back to 3% for the first time since March 2021. The rent component within shelter also grew at a slower pace last month, although market rents are falling in many markets across the country and this measure is likely overstated in the CPI itself. The food, health and personal care, recreation, education and reading, and alcoholic beverages, tobacco products and recreational cannabis categories all saw their annual inflation rate decline in May.

A particular focus for the Bank of Canada is its preferred measures of core inflation: CPI Trim and CPI Median. Both of these metrics, which strip out the most volatile components of inflation, sat at 3.0% in May, down from 3.1% in April. This is a positive directional change for the Bank, and they will be looking for more progress when the June CPI is released on July 15th.

The inflation data continue to give somewhat mixed signals. Headline inflation remains in check and is likely to remain near—but likely below—the Bank’s 2% target for the foreseeable future. Core measures of inflation remain somewhat elevated, and impacts from tariffs and counter-tariffs are likely still to be felt in the months ahead. The Bank must consider these factors, along with a weak labour market that has already begun to feel the effects of tariffs, as well as slowing population growth, which impacts both the supply and demand sides of the economy.

The Bank noted in its most recent rate announcement on June 4th that it “will support economic growth while ensuring inflation remains well controlled”, which signals a willingness to lower its policy rate if the Governing Council feel it is warranted. In our view, reducing the policy rate by 25 basis points on July 30th will indeed be warranted, with the picture becoming clearer after the June CPI and Labour Force Survey data releases.