Canada’s labour market had been following a notable trend of late: one where the overall market was responding to restrictive monetary policy through rising unemployment, while the backdrop of record population growth was also boosting employment. We’ve discussed previously how an exploding Canadian population has been the primary reason for employment growth, and that when viewed across a spectrum of indicators, it’s clear the overall labour market had been weakening for the better part of a year.

The latest Labour Force Survey data for March reveal a deviation from that trend. While population growth has remained robust—in fact, in the first quarter of 2024 the number of working-aged people added in Canada in Q1 2024 was 47% higher than during the same period in 2023—the deviation came in the form of the economy shedding 2,000 jobs in March, the first net loss in any month since last July. Those job losses were also paired with a growth of 91,000 people, of which 58,000 joined the labour force, which translates into an increase of 60,000 unemployed people and brings the unemployment rate to 6.1%, its highest level since January 2022.

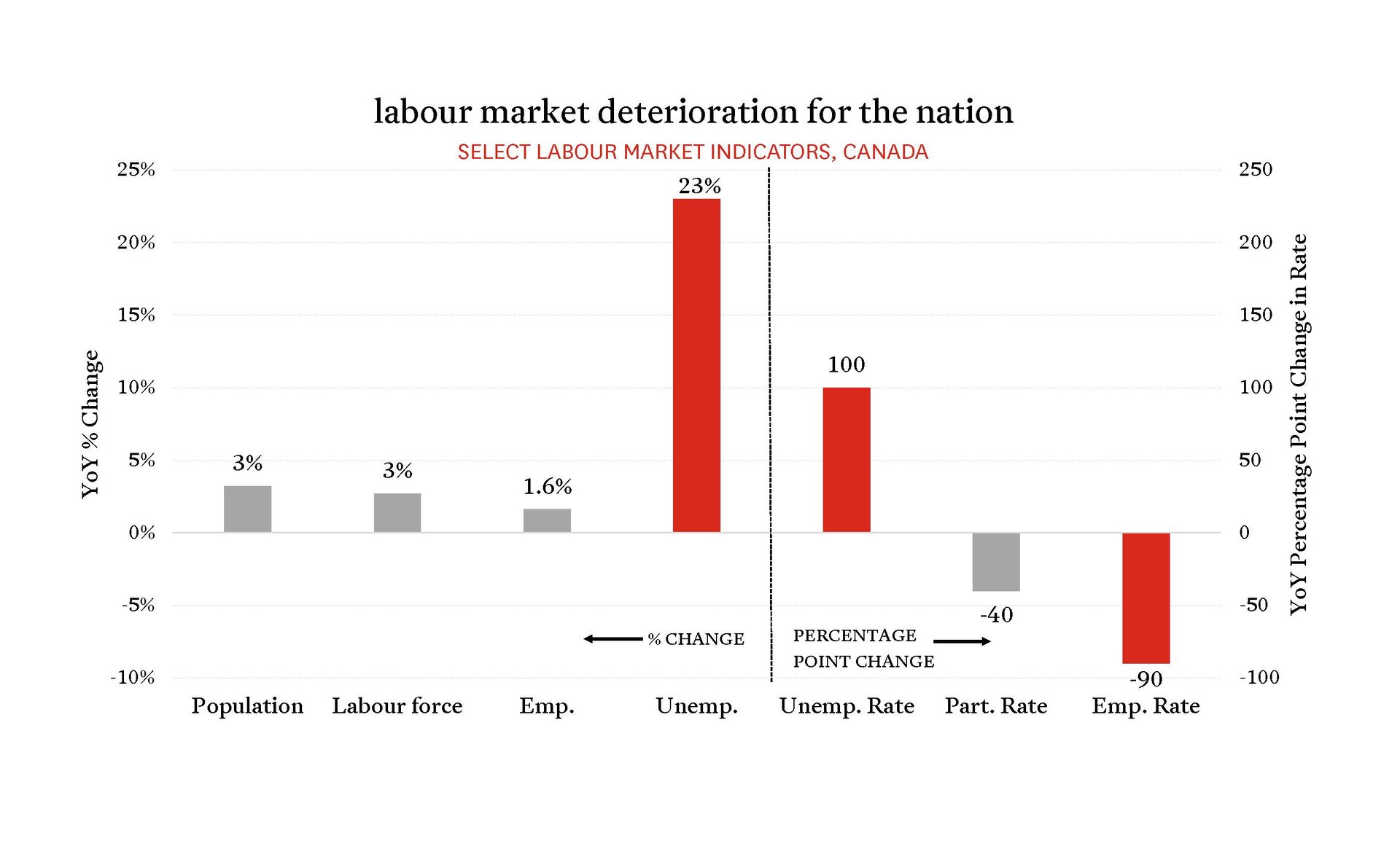

The weakness in the labour market is quite pronounced when viewed over the past 12 months. Unemployment has risen sharply over the past year, up 23%, while employment is up just 1.6%. The unemployment rate has increased by 100 percentage points, as both the employment rate and participation rates have declined.

Overall, the data point to a labour market burdened by high interest rates, which is in clear contrast to what’s happening in the US. The economy has responded to high interest rates in a number of ways, with inflation now inside the Bank of Canada’s target range (and inflation excluding mortgage interest sitting below target, at 1.9%), mortgage debt service ratios at an all-time high, per-capita retail spending declining, and per-capita GDP declining, among others.

It’s clear that the restrictive monetary policy undertaken by the Bank of Canada has achieved its goal. And with the effect of interest rate decisions coming with an 18-to-24-month lag, the time is now for the Bank to begin cutting its trend-setting rate.