This article is a section of the Spring 2026 edition of the rennie landscape, our semiannual report on the forces shaping housing markets in Metro Vancouver and across our key markets.

Each section of the landscape explores a different piece of the broader story—from interest rates and the economy to demographics, credit, and housing. Together, they provide context for understanding how these factors interact and what they mean for Metro Vancouver’s housing market.

Inflation has been under control for more than two years and interest rates have fallen. A new war, however, has caused energy prices to spike, and will raise inflation with it.

How Low Can You Go?

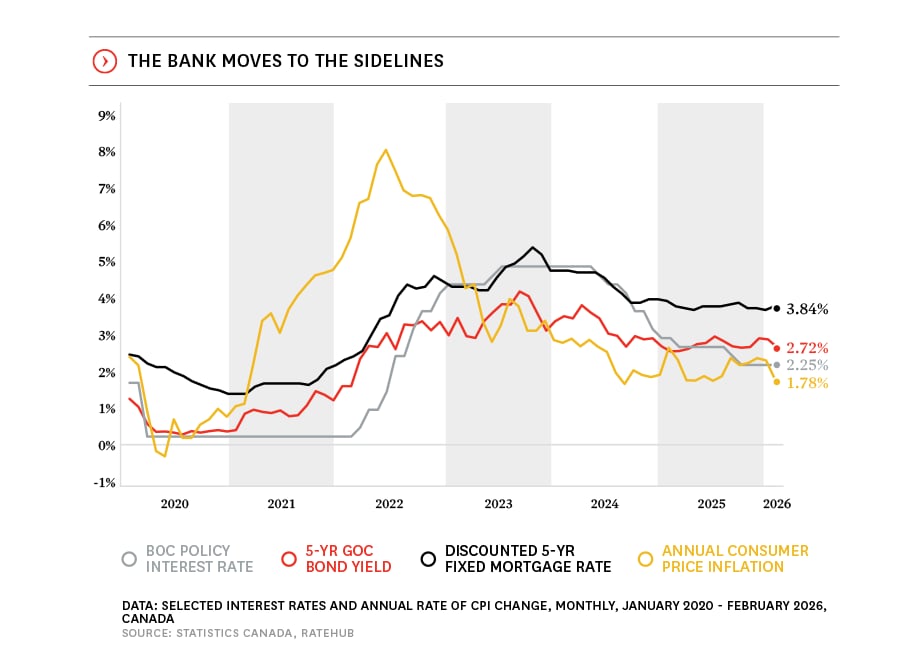

For a brief period, the era of watching inflation like a hawk and parsing through the minutiae of each inflation data release was finally behind us (those of us on the west coast who were refreshing the Statistics Canada website at 5:30 am were particularly thankful). Low and stable inflation had returned, with headline inflation remaining inside the Bank of Canada’s target range of 1-3% for more than two years and the Bank’s preferred measures of core inflation having remained below 3%. That paved the way for the Bank to lower its policy rate from 3.00% at the end of 2024 to 2.25% in September, where it has held it since.

In March, however, a war in the Middle East caused oil and gas prices to spike. Headline inflation will increase, and as the conflict carries on, high transportation costs will put upward pressure on prices of all manner of goods. Bond yields have already begun to rise in response to the conflict and fixed mortgage rates will follow. The labour market, as we noted earlier, has not been faring well and there is little to suggest any demand-side momentum in the economy that could put upward pressure on inflation this year.

This puts the Bank of Canada in a difficult position, with a relatively weak economy and rising inflation. Central banks can’t do anything to tame energy prices, which are set globally, but ours will monitor the effects of the conflict along with tariffs and any changes to trade policy. The likelihood that the overnight rate will be raised in the coming months has grown, but for the time being, the Bank will watch to see how the conflict evolves and how it impacts inflation.

Adding to the Supply of Debt

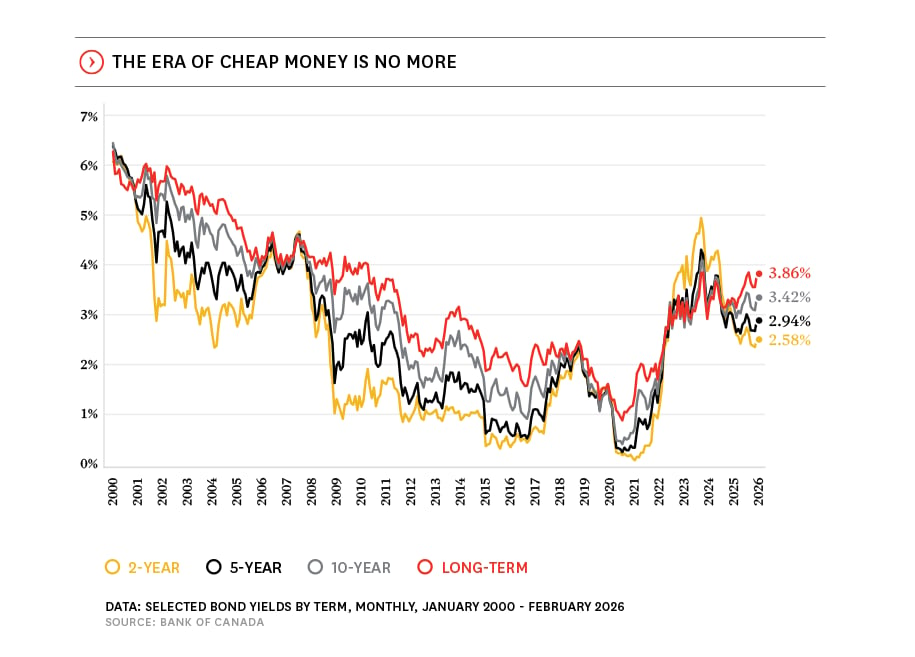

The yield curve normalized as low and stable inflation returned. Bond yields, however, are starting to rise as the conflict in the Middle East sends energy prices skyward.

For most of this century Canada has been in a declining interest rate environment as inflation was well-anchored (including averaging a bit less than 2.0% for the decade preceding the pandemic). The Bank of Canada kept its policy rate historically low, including lowering it in response to the Great Financial Crisis in 2008, falling oil prices in 2015, and the pandemic in 2020. Meanwhile government deficits, at least here in Canada, were relatively modest. The Bank's policy rate and bond yields both rose abruptly in 2022 in response to high inflation, and for most of 2023 and 2024 the yield curve was inverted, often a precursor to a recession.

We avoided the technical recession in Canada, but we’re faced with much higher yields than just prior to the pandemic even as low and stable inflation had returned. With a new conflict in the Middle East causing oil prices to spike, bond yields have started to rise in March. Additionally, tariffs, disrupted trade f lows and supply chains will continue to put added pressure on prices. Record government deficits (which we will discuss further in the Credit and Debt section) will also contribute to inflationary pressures and increase the supply of bonds, pushing prices lower and yields higher in the months to come, raising fixed mortgage rates along with them.

Subscribe to rennie intelligence to read the full 2026 Spring rennie Landscape Vancouver report.