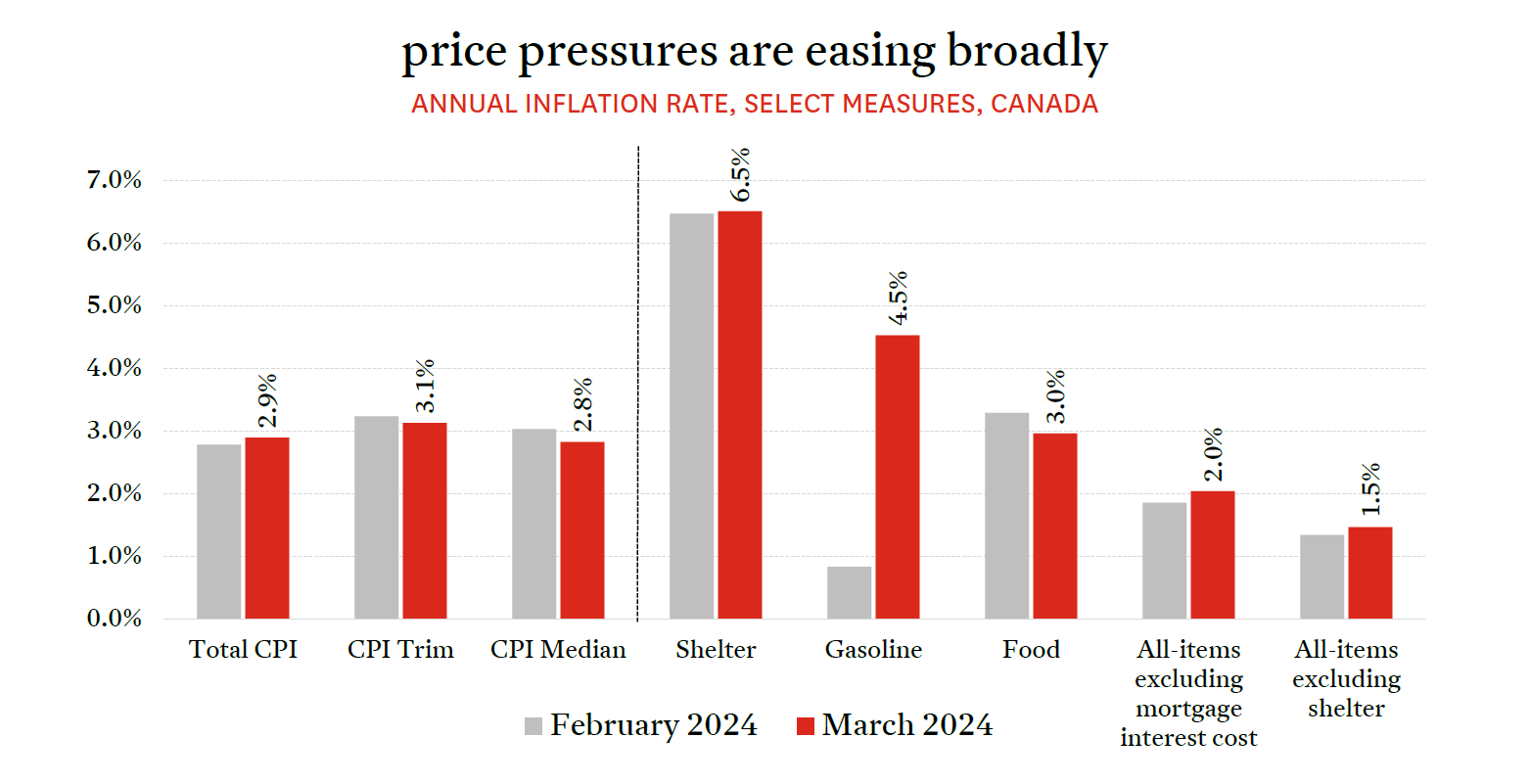

The latest release of Consumer Price Index (CPI) data from Statistics Canada saw a reversal of recent trends in headline inflation. Overall, the annual rate of inflation ticked up in March, to 2.9%, after two consecutive monthly decreases. However, in spite of the directional change to the headline rate, there’s a lot of good news for consumers (and the Bank of Canada) underneath the hood of the total CPI.

Core measures of inflation, which strip out the most volatile components of the index, all declined again last month and CPI Median is now within the Bank’s target range. Additionally, the 3-month annualized average for both CPI Trim and Median (1.1% & 1.4%, respectively) are clearly showing price increases that are decelerating recently. The Bank had previously been pointing to these specific calculations for being too elevated and being an indicator that inflation had not subsided enough. There are now clear signs that not only have price increases moderated broadly across the CPI, but that they have slowed significantly in recent months.

The big reason for the increase in the CPI last month won’t come as much of a shock to anyone who’s had to fill their gas tank in recent weeks, as oil and gas prices have spiked of late. Energy prices, which are set on global markets and are outside the control of the Bank of Canada and its monetary policy, were responsible for the biggest shift month-to-month in March and are notoriously volatile.

Shelter inflation, which was unchanged last month at 6.5%, remains the biggest contributor to the overall rate and is being driven by two things–mortgage interest costs and rent–that both of these components are being directly fueled by high interest rates. Holding interest rates higher for longer won’t do anything to help bring these aspects of inflation back down, and will continue to put stress on an undersupplied housing market–both ownership and rental.

With other metrics showing an economy slumping under the weight of high interest rates–particularly the labour market–the March inflation data show that the time has already come for the Bank of Canada to cut its policy rate. While it is our view that the Bank erred in maintaining the rate on April 10th, the latest data reinforces the need for a cut on June 5th.