The traditional data sources on which we rely to evaluate and understand our local real estate market are almost exclusively focused on events that have occurred in the past. Whether it’s measures such as sales, listings, or prices, they each tell us about what has already happened, when, and where. What these metrics don’t tell us though, is why things are happening the way they are and what is going to happen in the future. With this in mind, and to gain insights into why buyers and sellers are, or are not, participating in real estate and what their future intentions might be, we’ve been conducting semi-annual Consumer Sentiment Surveys (in partnership with the Mustel Group) since 2021.

We’ve asked respondents, surveyed throughout Metro Vancouver, about their intentions to buy or sell a home and their challenges when participating in the real estate market. We also asked them about their expectations of things like their personal financial situation, mortgage rates, home values, and whether it will be a better time to buy or sell in the future. Additionally, we asked how high interest rates are affecting their real estate decisions and personal finances. Their responses provide both a snapshot of consumer sentiment at a point in time, but—most importantly—how their expectations and intentions are evolving.

Understanding sentiment, expectations, and intentions is critical, as these ultimately govern behaviour—each on their own and together. The Bank of Canada monitors consumer and business expectations of inflation, as inflation expectations in and of themselves influence actual inflation. For example, when consumers (or businesses) expect prices to rise, they are more likely to be willing to spend more, thus fueling actual inflation. Similarly, when consumers expect real estate values to increase in the future, they demonstrate a greater desire to buy—thus applying upward pressure to prices. And while intentions don’t always translate to action (for example, I intend to go to the gym tomorrow morning), they do serve as a useful barometer of the consumer mindset and a window into potential future behaviour.

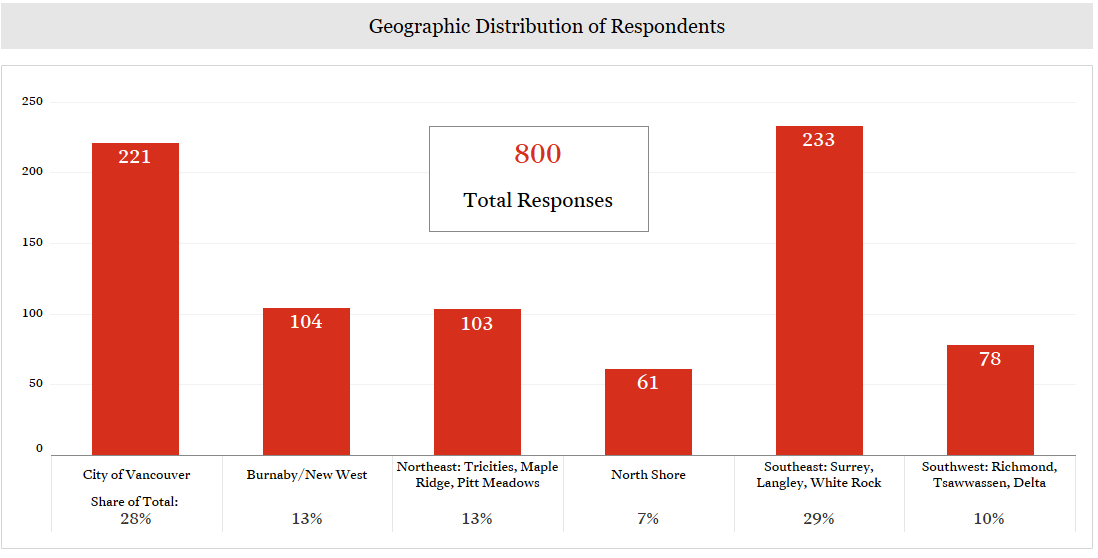

In the most recent iteration of our Consumer Sentiment Survey, conducted in Q4 2023, we spoke to 800 people in Metro Vancouver, broken down by area as follows:

Responses were then sample-weighted by age within gender and regional sub-market to match Statistics Canada’s data for each sub-market.

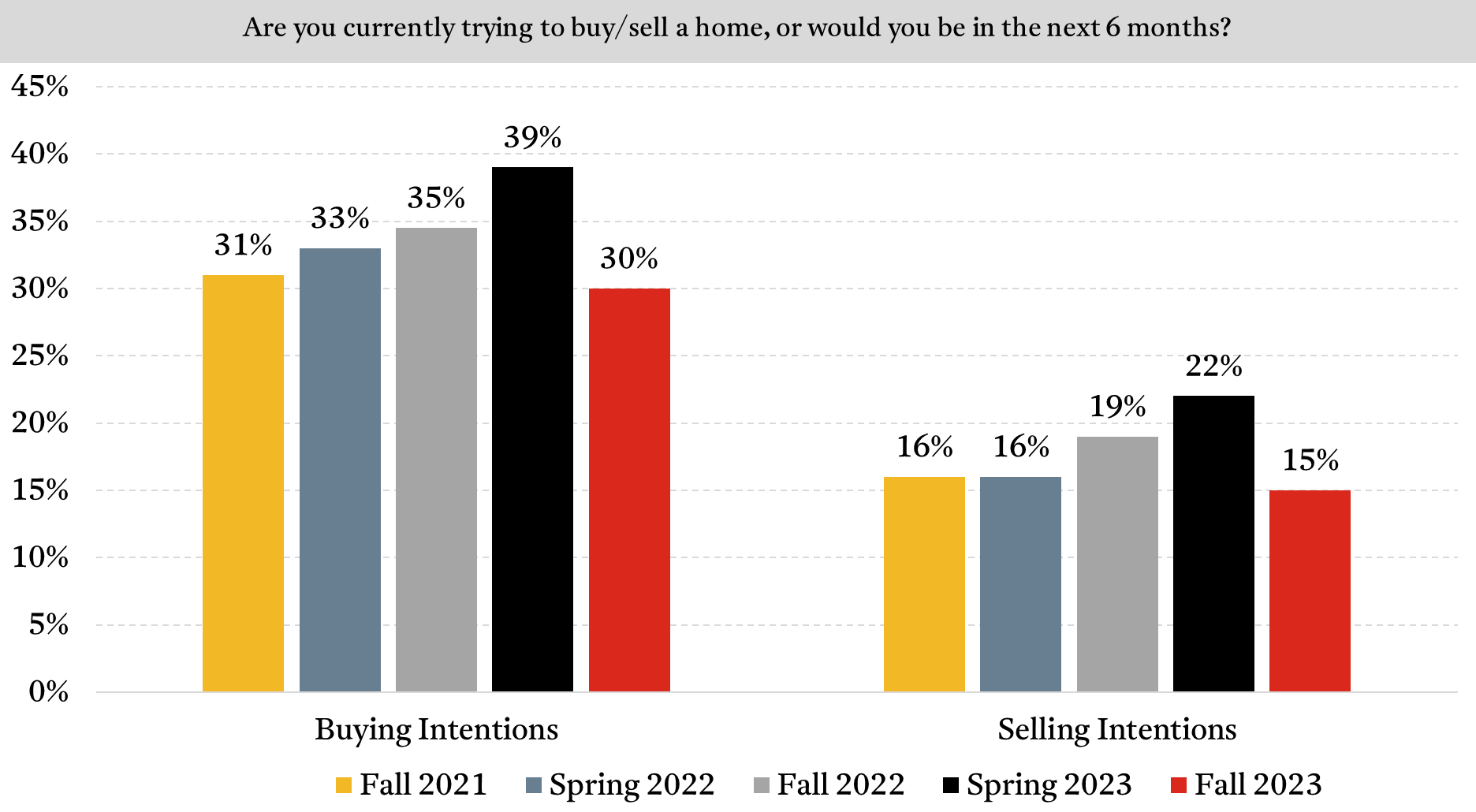

Decreasingly Intentional

The proportion of respondents indicating an intention to buy a home (either to live in or for investment) has remained remarkably high through the first five iterations of our survey, even as the macroeconomic landscape has changed dramatically over that time period. And while buying intentions did increase through the first two years of the survey, more recently they declined to 30%. That said, nearly a third of adults in Metro Vancouver are still interested in buying a home in the next six months, and although not all of those people ultimately will purchase in that time period, it still represents a significant pool of unmet demand. To flesh it out a bit, 30% of respondents translates into an absurdly high 355,000 households regionally, which would be the equivalent of more than five years worth of transactions in Metro Vancouver (MLS and pre-sale combined). This still tells us something important, though: that Metro Vancouver residents remain resilient in their intention to purchase real estate, even as rising and high interest rates have eroded affordability.

When we segment across respondent types, a few groups stand out. More than half of younger adults—52% of those aged 18-34—indicated an intention to buy, as well as 40% of renters. These younger, renter groups are eager to participate in real estate but are also the most challenged by affordability (more on that later).

Selling intentions, meanwhile, have been consistently lower than buying intentions over the past two and a half years. This suggests a relative imbalance between demand and supply and provides some insight into the low levels of inventory observed in the resale market the last few years; simply put, there are fewer would-be sellers than would-be buyers. Selling intentions have also been decreasing of late, with those respondents indicating a desire to sell in the next six months declining to 15% in the most recent iteration of the survey.

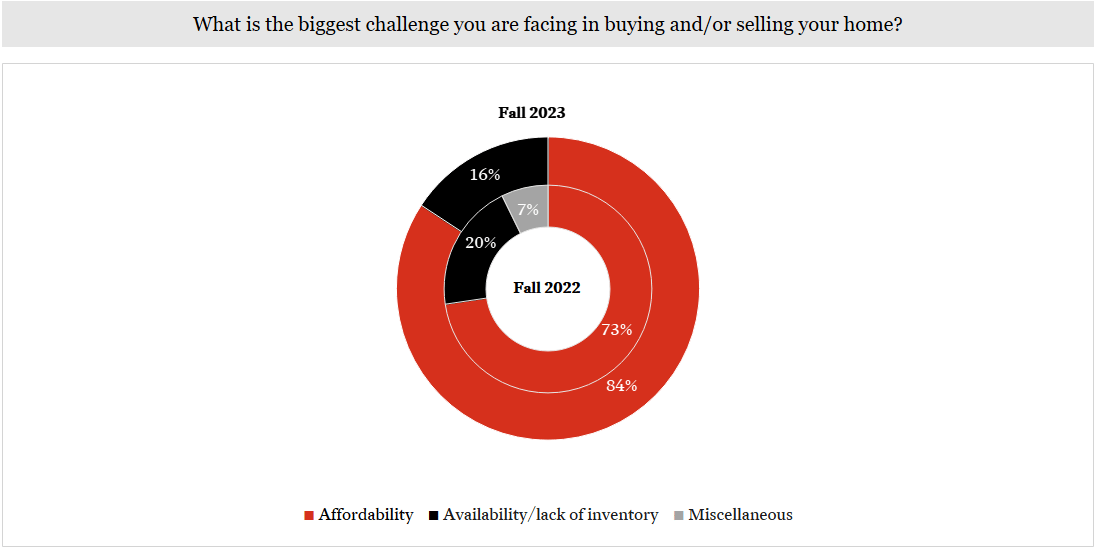

There are a number of obstacles buyers and sellers face when deciding whether or not to participate in the real estate market, but the overwhelming majority of respondents say that affordability is the biggest challenge: in our most recent survey, 84% of all respondents indicated as much. But when we segment owners from renters, we find that “only” 82% of owners felt affordability was their main concern. This is a high number to be sure, but it’s less because those who own likely have equity in their current home to lean on when determining whether or not to participate further in the market. And depending on how long someone has owned their property, they may have accumulated substantial equity along the way as home values, on average, have risen 85% in Metro Vancouver over the past decade. On the other hand, 94% of renters cite affordability as their major challenge, which makes sense as they haven’t capitalized on the benefits of rising prices—in fact, it’s been quite the opposite.

And what’s more, since the Bank of Canada embarked on their campaign to raise interest rates in early 2022, affordability has been significantly eroded. To put it in perspective, a 25% decline in home prices would offset a 250 basis-point increase in the cost of borrowing in order to keep mortgage payments constant (notwithstanding changing down payments). The Bank of Canada has raised its policy rate 475 basis points since March 2022, which would require a corresponding 41% decline in home prices to keep affordability constant. Instead, the composite benchmark price has declined only 11% over that time, which would correspond to 51% higher payments. And if you consider the benchmark price for condos, the logical entry-point for a first-time buyer, they have declined even less (by 4%), resulting in payments that are 63% higher for a comparable property.

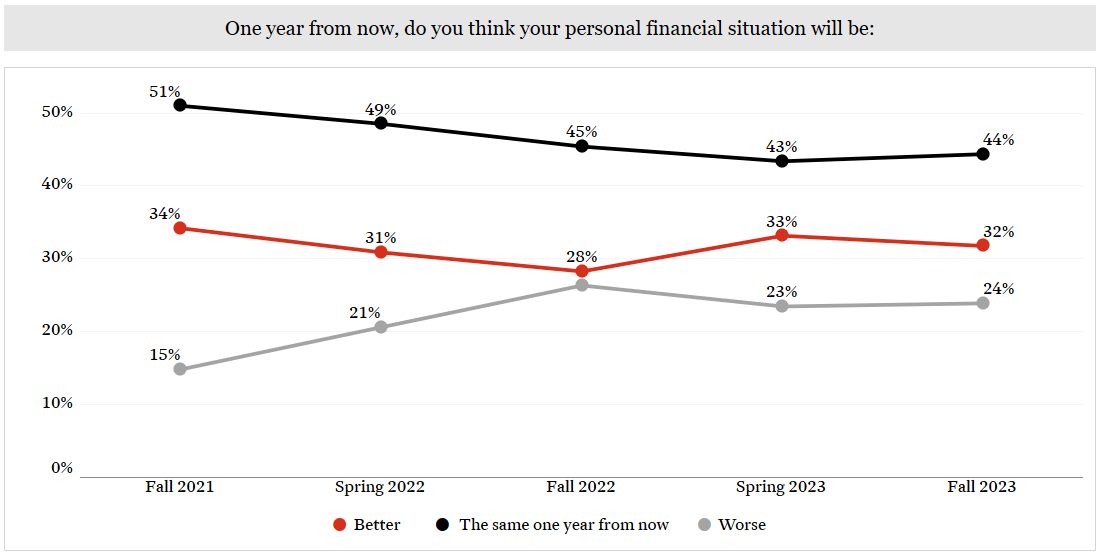

A Mix of Optimism and Pessimism on the Year Ahead

One notable positive that came from our last two consumer sentiment surveys is the insights gained into respondents’ personal finances. Responses to the question of what people expect their personal financial situation to be in a year had been increasingly negative through 2022 in the face of high inflation and rising interest rates. Most recently, however, as inflation has been slowing, the proportion of respondents who expect to be in a better financial position from our most recent survey increased to 33% in Q2 2023 before declining marginally to 32% most recently. Meanwhile, those who expected to be worse off increased to 24% but was still below its peak of 26% from one year ago.

When we break it down by age groups a clear trend emerges, namely that younger adults are most optimistic about improving finances. In the 18-34 age group, 50% expect to be better off in a year, compared with just 32% of 35-54 year olds and 17% of those 55+. This makes sense, with younger adults being in earlier stages of their careers and often experiencing rising incomes, while older adults may experience more income stability (that is, less variation year-to-year). This optimism about an improving financial situation likely impacts the desire to purchase real estate and is one factor in the high rates of buying intentions among the 18-34 age group as well.

When we ask consumers about where they think mortgage rates are headed, one thing is clear: no one really knows. This is certainly in line with economists’ forecasts, where there is also no clear consensus (and plenty of incorrect predictions). In both interactions of the survey in 2023 there has been a substantial, if unexpected, departure from past versions of the survey where there was near unanimity that rates were going to increase. And they did! As we mentioned, the Bank of Canada has raised its policy rate 10 times since March 2022, in turn increasing variable interest rates. Fixed interest rates, meanwhile, are influenced by bond yields, which had been increasing steadily since early 2021 before peaking in October. With 41% of respondents expecting mortgage rates to be higher next year, and 23% expecting them to lower, one might expect consumers' views on when might be a good time to buy real estate to be similarly fragmented. But mortgage rates are just one (important) factor influencing those perceptions (more on that later).

Mortgage rates are another topic where there is divergence among age groups. Younger adults, those aged 18-34 are far more likely to expect rates to be higher in one year, with 53% of them answering accordingly, Meanwhile, among those aged 35-54, only 33% expect higher rates in a year, along with only 40% of those aged 55+. It’s unclear exactly why older adults are more optimistic about mortgage rates in the near future—though to be clear, we have a strong expectation that rates will be lower 12 months from now—but perhaps having experienced past market cycles and different interest rate environments gives them confidence of changing dynamics in the near term.

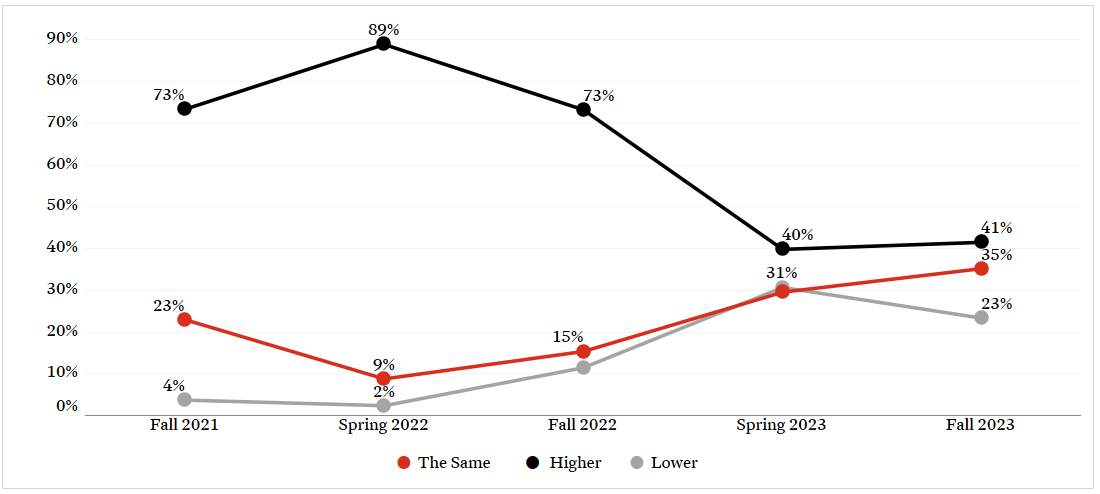

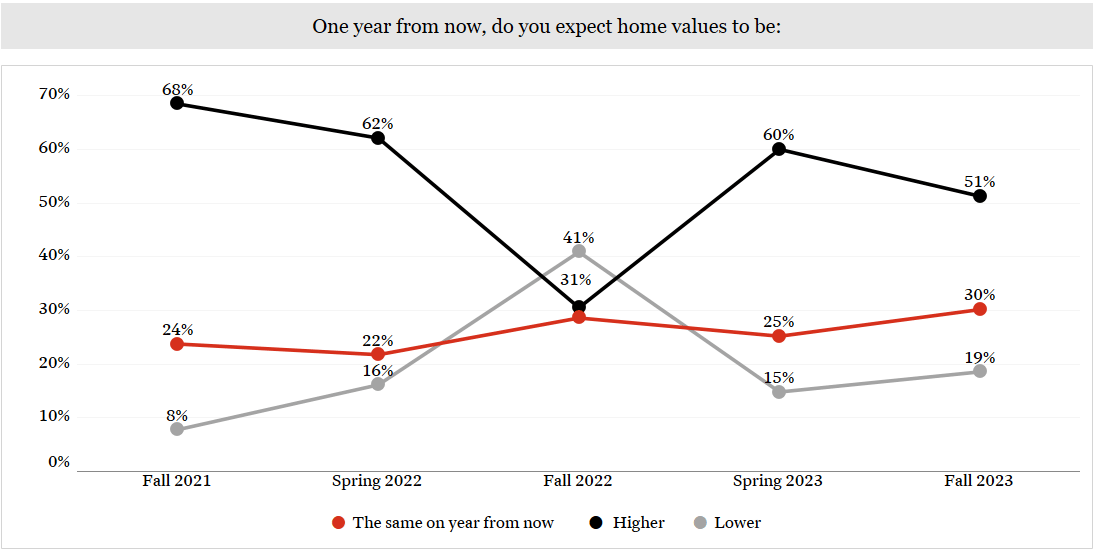

When we ask respondents about their views on where home values are going over the next 12 months, there have been interesting changes over the past two years of the survey. In Q2 2022, which was a time of rising home prices, 62% of respondents saw values being higher in a year while only 16% saw them being lower. Then when we asked again in Q4 2022, when prices were falling, 41% expected them to be lower in a year while 31% expected them to be higher. In the Q2 2023 survey, which was once again conducted during a period of rising prices, responses to this question reverted back to where they were one year earlier: 60% expected values to be higher in one year and only 15% expected them to be lower. And, most recently, during a period of marginally declining prices, the proportion of respondents who expect prices to be higher declined to 51%.

It makes sense that when prices are increasing the majority of residents in Metro Vancouver expect them to continue to increase in the short-term; similarly, when prices are decreasing, they expect them to continue to fall in the short-run. Predicting an inflection point in values is difficult, and looking at recent history to predict the future is quite common, if imperfect. These results also give us a window into what respondents think about what makes it a good or bad time to buy or sell real estate as we see in relation to the next survey question.

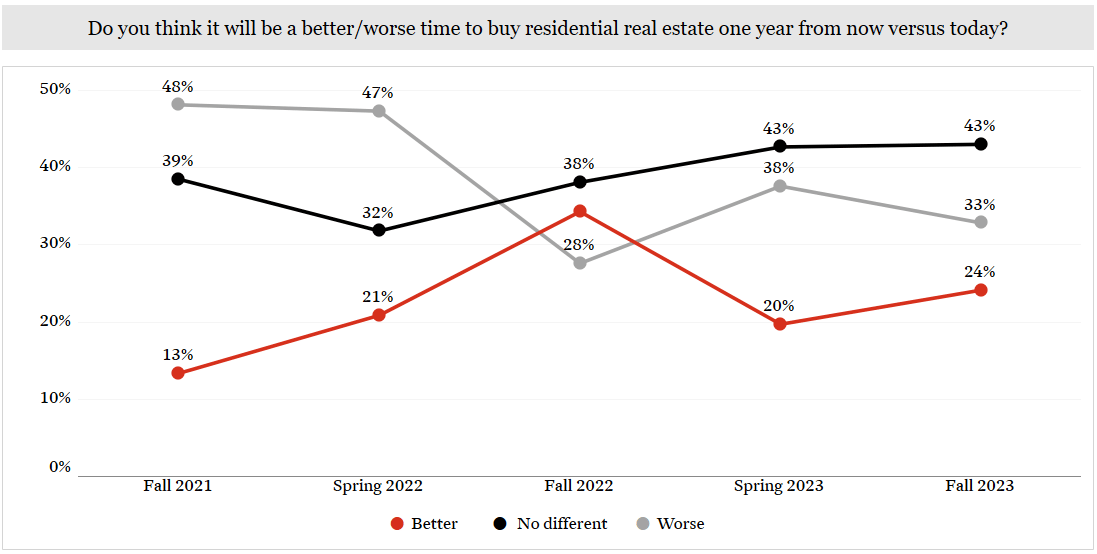

There is a strong correlation between respondents' views on where home values are going and when they think it will be or won’t be a good time to buy. Interestingly, the same correlation is not present in respondents’ views on where mortgage rates are going in relation to when it will or won’t be a good time to buy. In the three most recent survey results, the most common response is that it will be no better or worse to buy residential real estate in one year. But the proportion of respondents who think it will be a worse time to buy, declined from 47% in Q2 2022, to 28% in Q4 2022, before rebounding in 2023 with the most recent result at 33%. This follows a similar trajectory as those who think values will be increasing over the next year. Relatedly, those who think it will be a better time to buy in one year increased from 21% in Q2 2022 to 34% in Q4 2022 before declining in Q2 2023, with 24% in Q4 2023 thinking next year will be a better time to buy.

What this suggests is that prices and how those prices are changing are—far more than interest rates—affecting consumers' perceptions of when it is a good time to buy residential real estate. This is intuitive: when values are increasing, there is urgency on the part of buyers to buy now before prices rise further; in contrast, when values are decreasing, buyers would rather be patient and wait for prices to fall more. Of course, mortgage rates still play a key role in buyers' ability to actually afford to purchase real estate, as do buyers’ ongoing financial situations (as we’ll see in the section ahead).

Feeling the Weight of High Rates

Another important factor in the decision to buy real estate is job security. While income is a major driver of how much a borrower can afford, job security is an important factor influencing a potential homebuyer’s willingness to commit to a 25-year (or longer) amortization on a mortgage. And so with a labour market that has been weakening of late—the unemployment rate in Metro Vancouver is now up to 5.8% from a low of 3.9% in September 2022—we asked respondents in the most recent iteration of the survey if they’re concerned about their job security now or in the near future. With this being the first time we’ve asked this particular question (meaning we don’t have a historical time series to look back on for context), we can see that a sizeable proportion of respondents are indeed concerned about their job security, with 39% indicating they’re either a little or lot concerned.

Once again, when we segment these results by age, we see significant disparity in the responses. And again we see younger adults facing greater challenges, with 48% of those aged 18-34 telling us that they are concerned about job security, compared with 37% of those aged 35-54 and just 26% of those 55+. Given that younger adults are in the earlier stages of their career, these results aren’t necessarily surprising, but once again they show another hurdle that the group faces in their quest to attain homeownership.

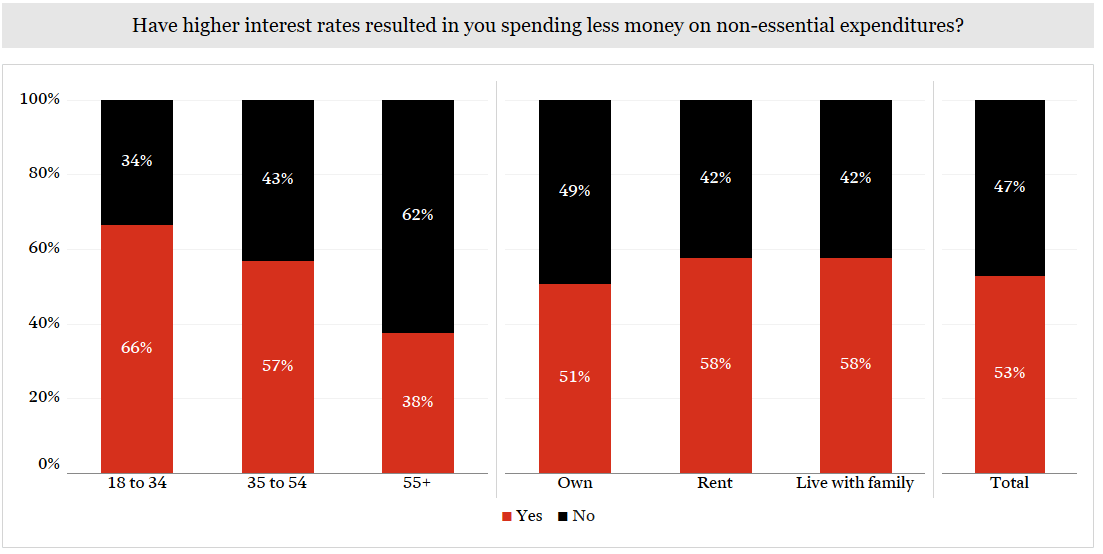

Looking at how higher interest rates have affected household spending, more than half of all respondents in Metro Vancouver have indicated that they are spending less on non-essential items due to higher interest rates. This reduction in non-essential spending is contributing to the disinflationary environment we find ourselves in today (most recently, headline inflation in Canada sits at 3.4%—a huge improvement from the generationally-high 8.1% back in June 2022) as consumers allocate more of their incomes to servicing debt, essential spending, and savings.

It’s the younger adults who’ve adjusted their spending patterns the most, with two-thirds of respondents already spending less on non-essentials, compared to 57% of 35-54 year olds and just 38% of those 55+.

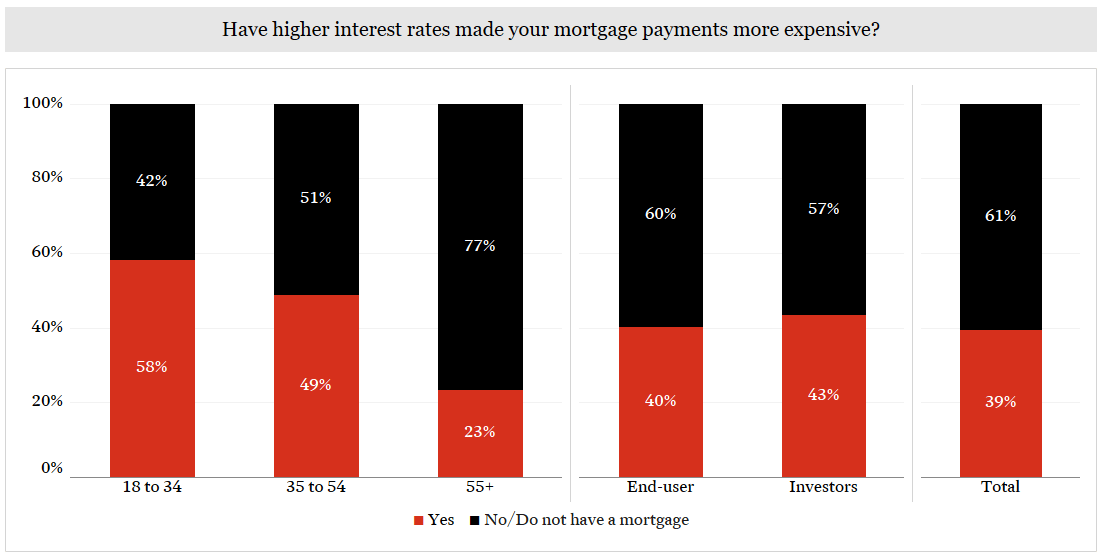

We asked homeowners if higher interest rates have made their mortgage more expensive and 39% answered yes. The other 61% either don’t have a mortgage or have a fixed-rate mortgage and have not yet had to renew. This is another area where younger adults are more acutely affected by higher interest rates, with 58% of 18-34 year olds answering yes, compared with 49% of 35-54 year olds and just 23% of 55 and over. Clearly, the full effects of the Bank of Canada’s prior rate tightening cycle have not yet been felt. Currently in Canada, two-thirds of all outstanding mortgage dollars are in fixed rate mortgages, so over time, as more Metro Vancouver homeowners go to renew their mortgages at higher rates, we could see these numbers rise.

As we’ve now turned the corner into 2024 and consider where the housing market in Metro Vancouver is headed, there are important takeaways we can glean from our latest consumer sentiment survey.

First and foremost, Metro Vancouver consumers still want to participate in their local real estate market, particularly on the buying side of the ledger. They face significant hurdles, especially in terms of affordability and high interest rates, but their answers show a clear desire to “get in” when they can. It’s also clear, however, that the weight of high interest rates (and inflation) has not been felt equally across the region, and that younger adults are increasingly bearing the brunt of the current macroeconomic environment. Younger consumers, in particular, will be hoping that interest rates ease and affordability improves so they can begin to participate in the market.

In the meantime, we will continue to watch the Bank of Canada, the market, and the economy while looking forward to our Q2 2024 survey results to once again assess how people are feeling about the housing market here in Metro Vancouver.