With the pace of housing market activity having declined sharply in the second half of 2022, the Vancouver Region is squarely in the midst of a dramatic slowdown—the likes of which we haven’t seen in a decade.

The housing market in Metro Vancouver, like most across the country, has been characterized by muted MLS sales counts of late, brought about by interest rate hikes that themselves were triggered by persistently high inflation. Meanwhile, a robust labour market has served to keep supply in check, even as sales have slowed, as the pace of new listings has been below typical levels (being highly correlated with sales counts, this doesn’t come as a huge surprise). Overall then, housing market activity has been sluggish into the fall—a time of year that typically sees an uptick in buying and selling.

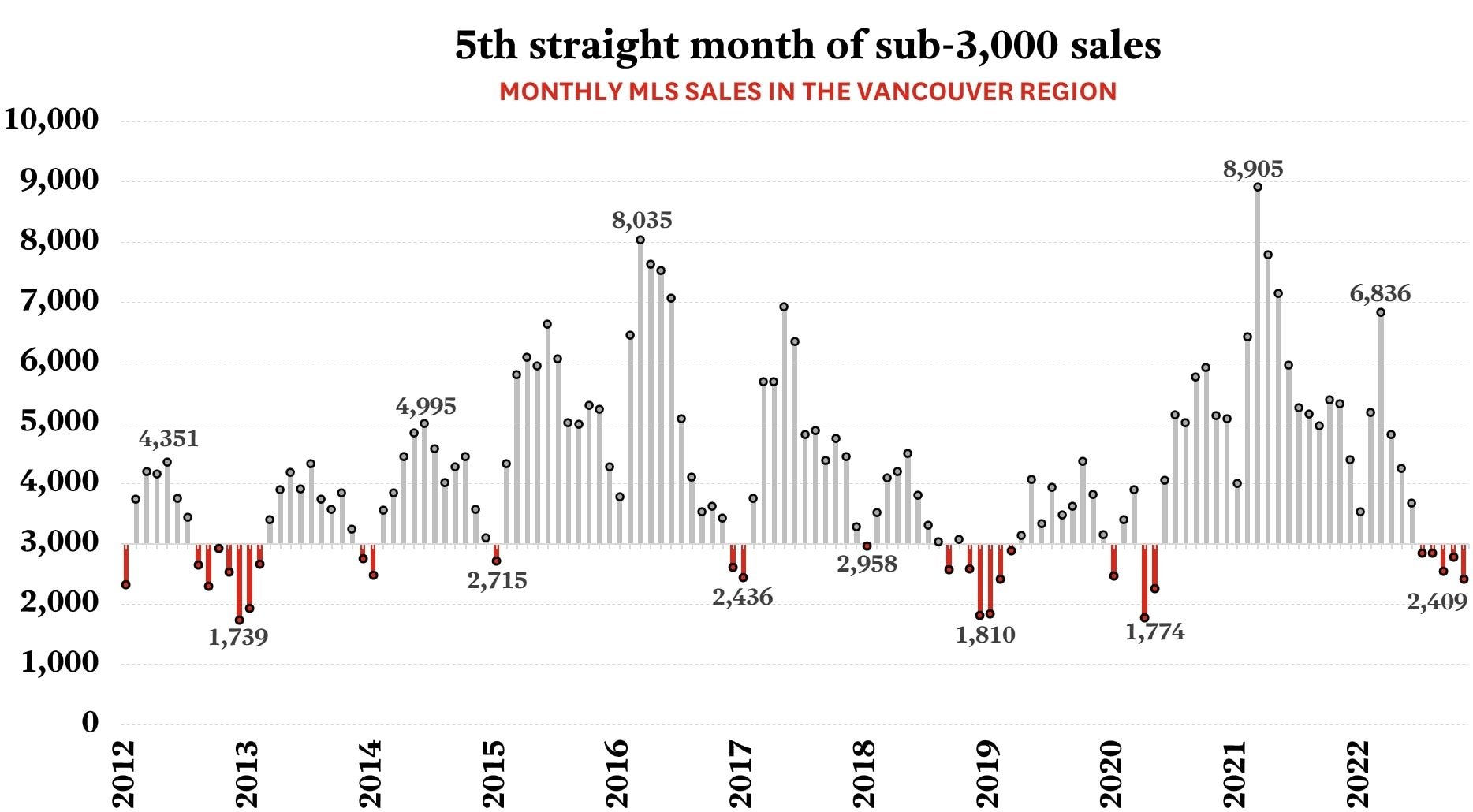

Normally, MLS sales counts in this region increase between September and October, followed by a decrease in November. In keeping with this trend, sales were in fact 9% higher in October than they were in September, and then 13% lower in November, thereby aligning perfectly with the typically-observed seasonal bump. Having said that, the actual count of sales in October and November fell far short of the norm: the 2,778 transactions in October were 36% below the past 10-year October average and the 2,409 sales in November were 39% below the past 10-year November average. Furthermore, the overall regional MLS sales count failed to surpass the 3,000-mark for the fifth consecutive month—something that hasn’t happened since early 2019.

The 3,000-sale threshold is one that is rarely missed in Metro Vancouver. Over the past 10 years, only 24 months failed to achieve the mark, including the most recent five.

We’re now part way through December, and on pace for fewer than 2,400 sales again this month, noting that the second half of December is typically much slower than the first half. If this plays out as expected, we will begin 2023 having registered six consecutive months of sub-3,000 sales—the most protracted period of slow sales in a decade (our market failed to reach the 3,000-sales mark over a seven-month period at the end of 2012 and into early 2013). And with current inventory levels sitting well below historic norms and the Bank of Canada having just increased interest rates a further 50 basis points on December 7th, it’s quite possible that this sales slump extends into the early part of 2023 before light appears at the end of the tunnel in the spring.

Our rennie intelligence team comprises our in-house demographer, senior economist, and market analysts. Together, they empower individuals, organizations, and institutions with data-driven market insight and analysis. Experts in urban land economics, community planning, shifting demographics, and real estate trends, their strategic research supports a comprehensive advisory service offering and forms the basis of frequent reports and public presentations. Their thoughtful and objective approach truly embodies the core values of rennie.