With spring upon us it’s time to check in on the latest iteration of the rennie consumer sentiment survey. We’ve been conducting the survey semi-annually since 2021 (in partnership with the Mustel Group) in order to better understand the “why’s” of our market. As traditional data sources around residential real estate are focused on what has already happened with metrics like sales and listings, sentiment helps us understand consumers' views and intentions, which in turn influence future behaviour.

We once again surveyed 800 people across Metro Vancouver in Q2 2024 about their views on a variety of topics related to our local housing market.

Waiting to Buy

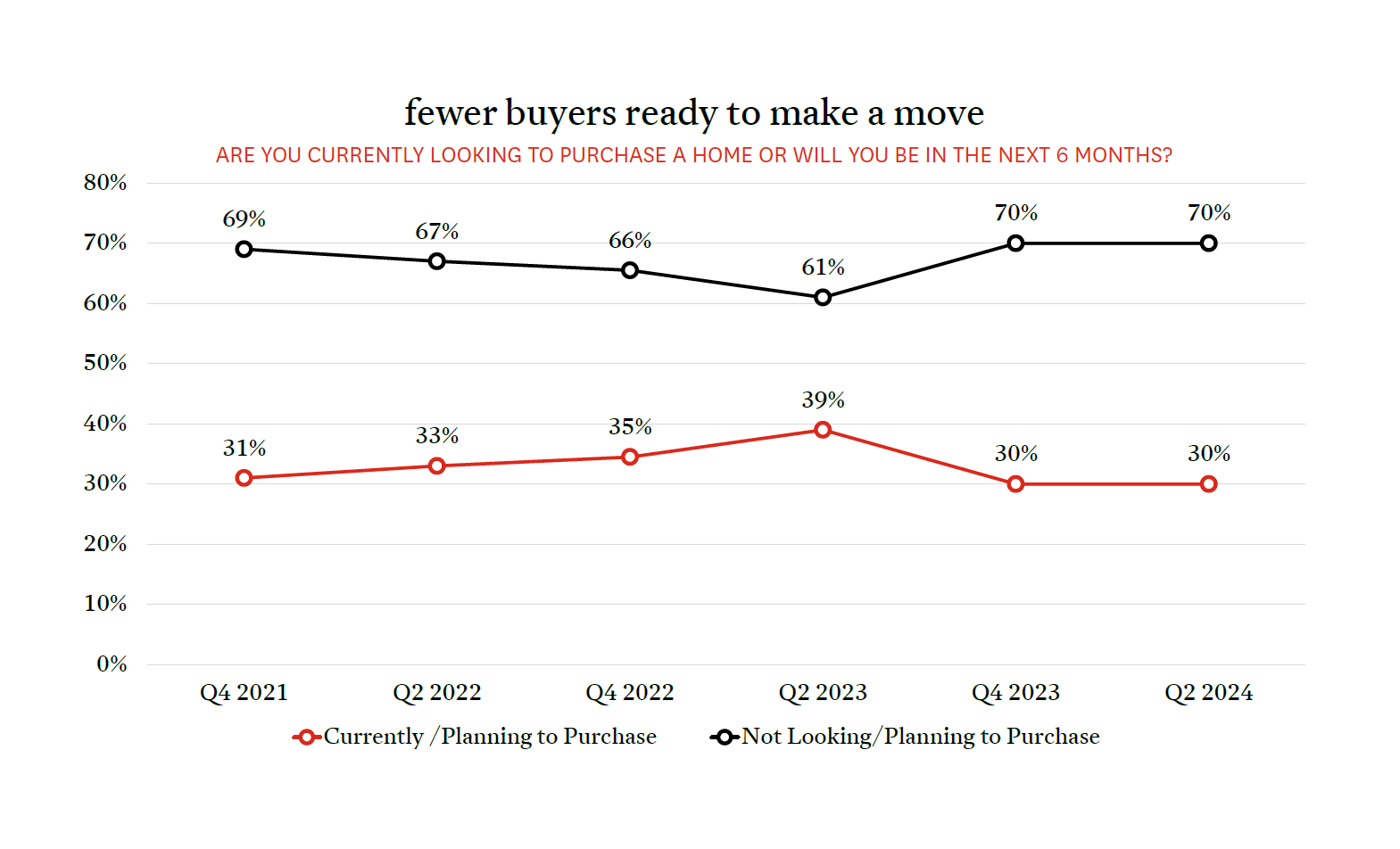

We noted in the previous iteration of our consumer sentiment survey that buying intentions—that is, the proportion of consumers who intend to buy a home in the next six months—had decreased for the first time since the beginning of the survey. And while they didn’t decline any further from the Q4 2023 to Q2 2024, they remained flat at 30%—again, at the lowest level since we began surveying consumers in 2021. With interest rates still at their highest level in a generation and affordability a top concern (75% of consumers report affordability as their biggest challenge), would-be buyers remain hesitant.

Looking Ahead for Rate Relief

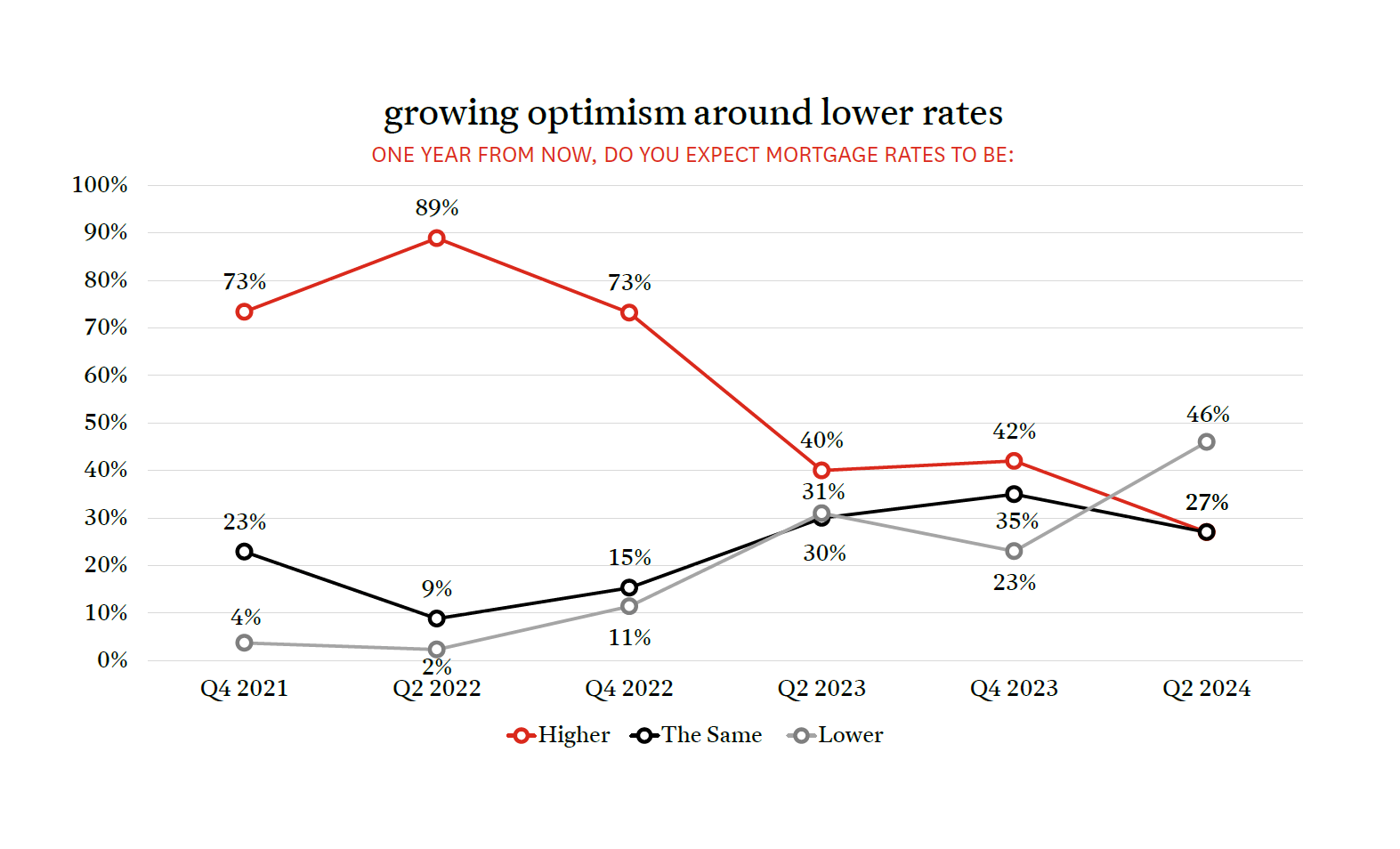

In 2023, consumers’ views on the path ahead for mortgage rates were unsurprisingly diverse given the level of uncertainty around inflation and the Bank of Canada’s response to it. With a bit more clarity on the path ahead, there has been a significant increase in the proportion of respondents who now believe that rates will be lower in one year compared to today. About half of consumers now agree with your author that the Bank of Canada will (and should) cut its policy rate in the months ahead. Given these expectations about a declining interest rate environment, it makes sense that fewer consumers are looking to buy a home in the near-term, and are instead waiting for interest rate relief before participating in the housing market.

As Rates Fall, Home Values Are Expected To Rise

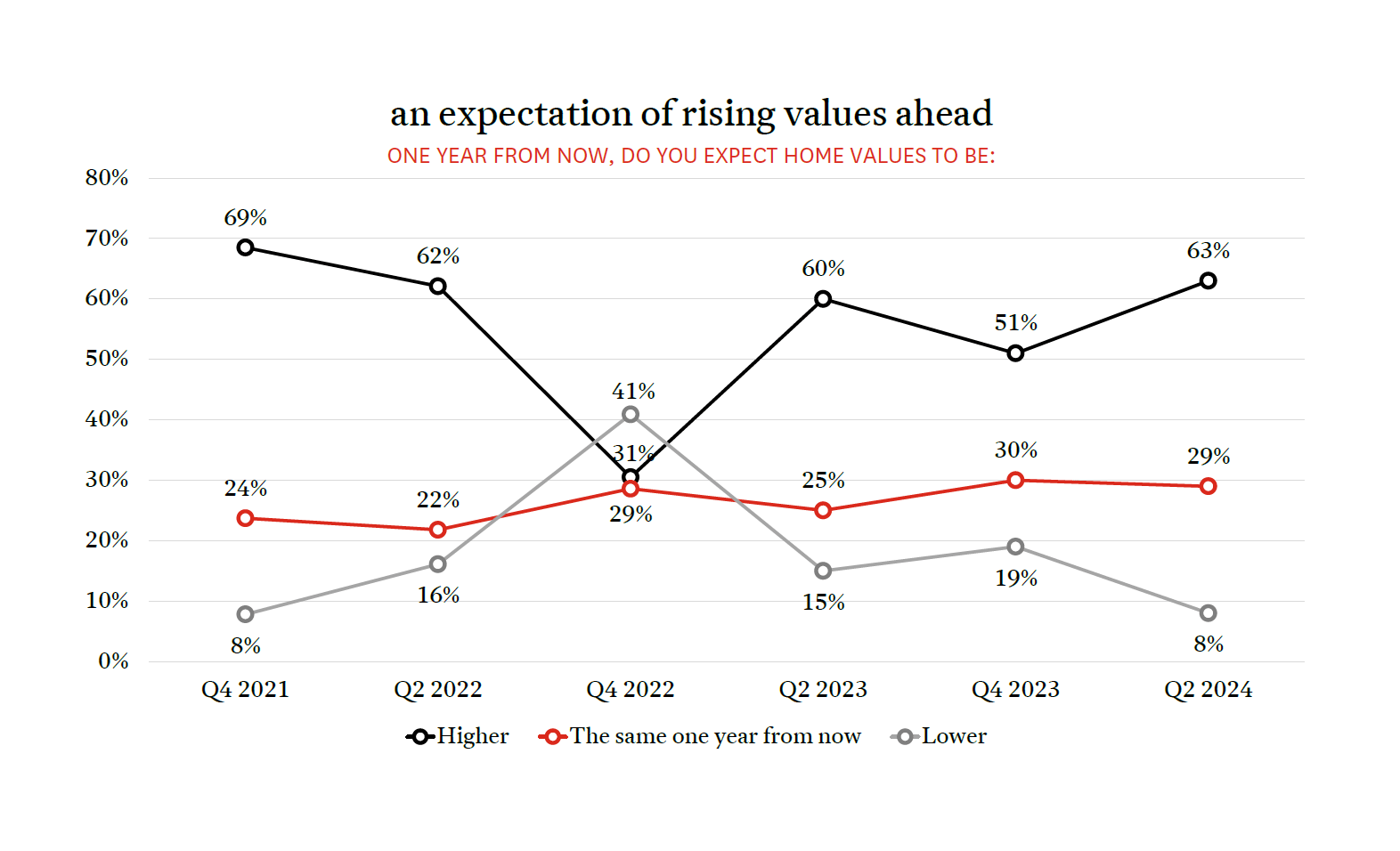

Respondents’ views on where home values are going over the next 12 months have seen some substantial shifts over the past three years, which is understandable given the changing dynamics of our local real estate market alongside rapidly-rising interest rates. With the aforementioned expectation that interest rates will be lower in one year, it makes sense that consumers expect values to rise over the same period. As declining interest rates improve affordability for buyers, some of that gain will likely be offset by rising prices. Interestingly, consumers' views on the direction of home values are now back to where they were in Q4 2021 and Q2 2022, when market conditions were substantially different from what they are today.

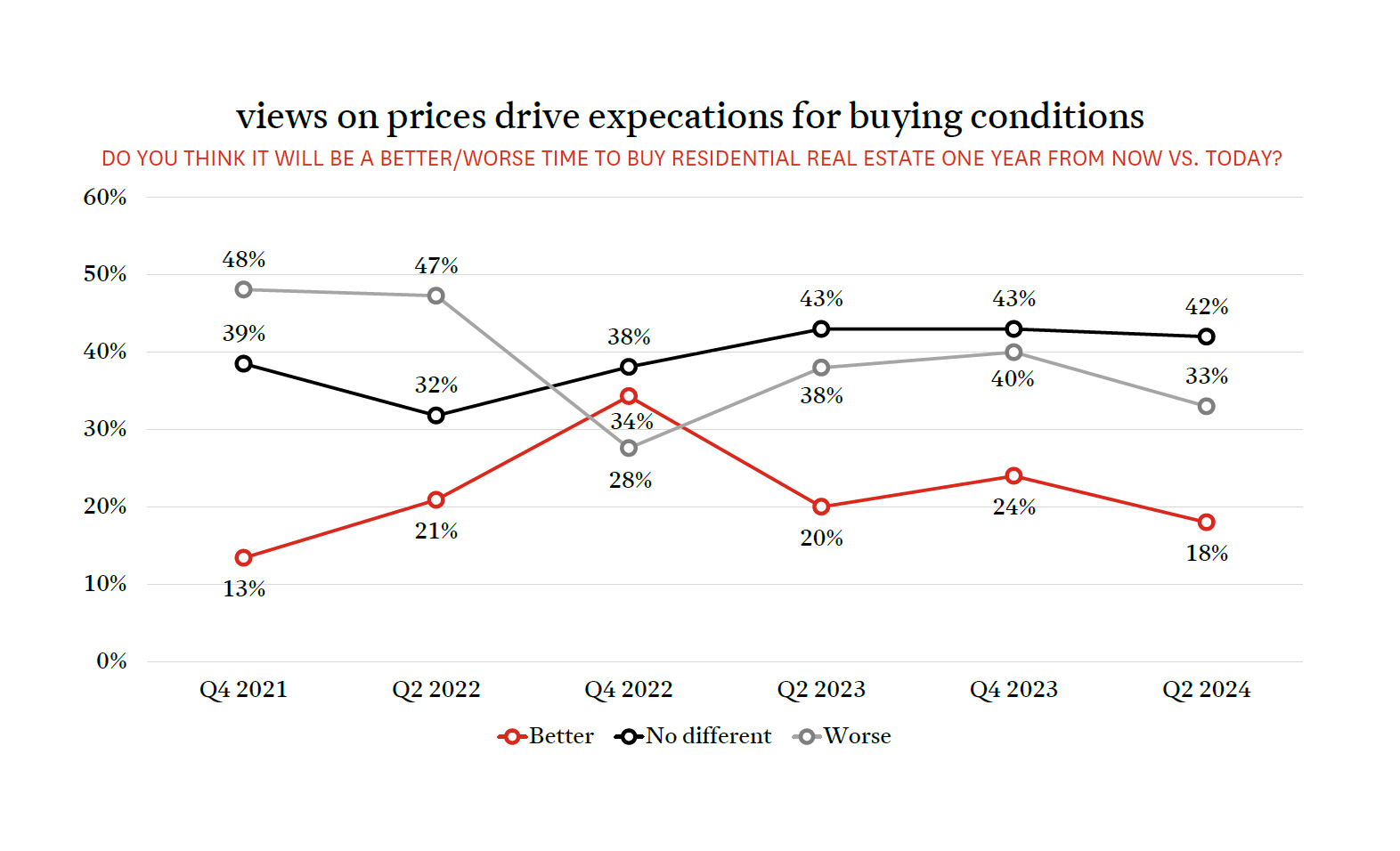

A Pessimistic View on Future Buying Conditions

There is a strong correlation between respondents' views on where home values are going and when they think it will be—or won’t be—a good time to buy. Interestingly, the same correlation is not present in respondents’ views on where mortgage rates are going. While the most common response is that it will be no better or worse to buy residential real estate in one year, there remains a higher proportion of respondents who think it will be a worse time to buy in one year (33%) than those who think it will be better (18%). As in past iterations of the survey, this suggests that prices and how those prices are changing are—far more than interest rates—affecting consumers' perceptions of when it is a good time to buy residential real estate. That consumers are silmultaneiously indicating that fewer of them intend to buy in the short term, even as they expect buying conditions to worsen over the next year, are in conflict with each other. Ultimately though, high interest rates today are likely the reason for that rationale.

Feeling the Weight of High Rates

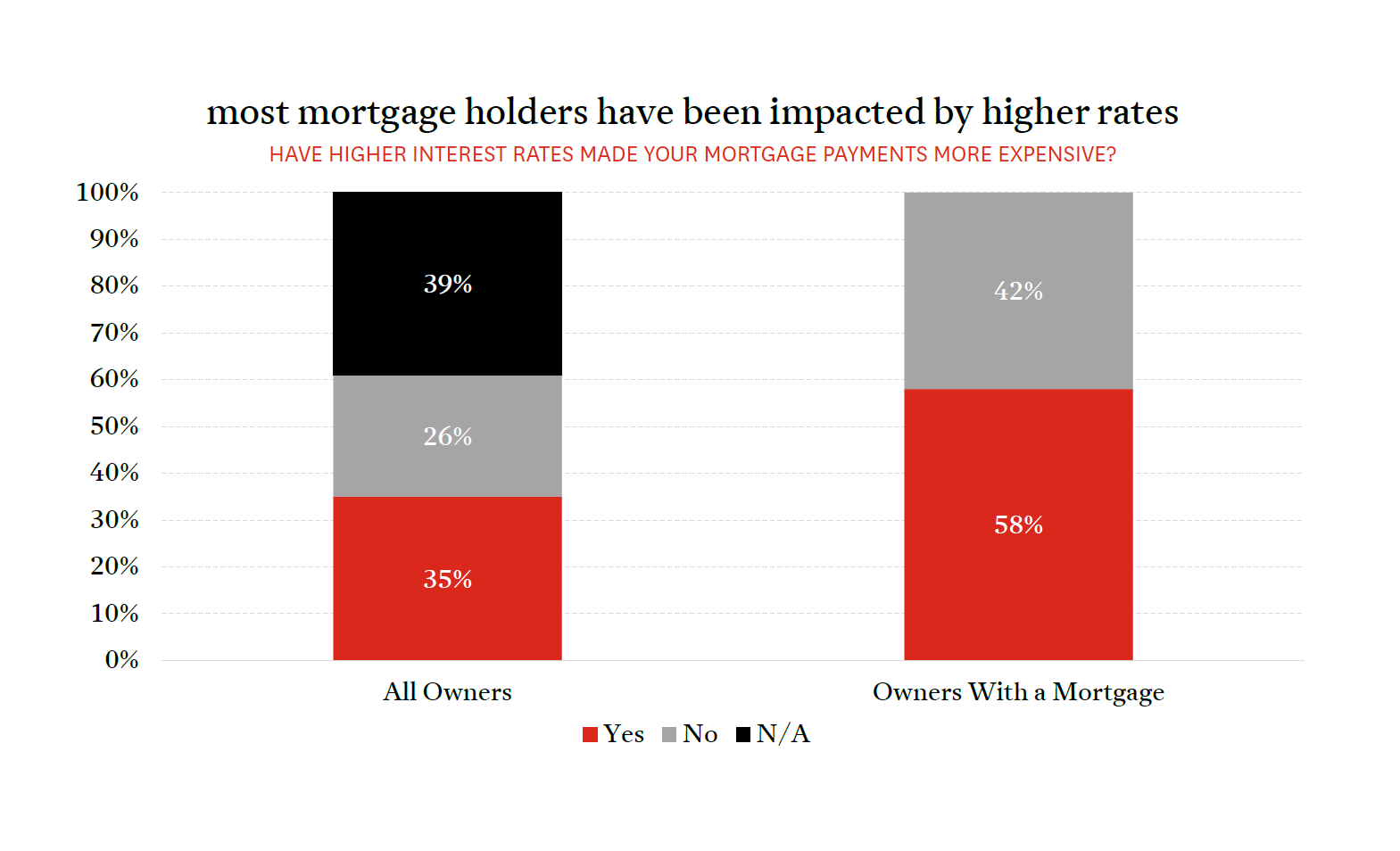

While the effects of high interest rates on homebuying activity are directly observable through traditional sales counts, the effects on existing homeowners are a little more difficult to quantify (unless perhaps you are a bank). As such we asked homeowners if high interest rates have made their mortgage payments more expensive to better understand the impacts so far, as well as the proportion of owners with a looming renewal on the horizon. More than half of owners with a mortgage (58%) have already seen their payments increase due to higher interest rates. This group will be a mix of fixed-rate owners who’ve already renewed their mortgages, and variable-rate holders with either variable payments or fixed payments but had previously hit their trigger rate. The remaining 42% of mortgage holders that have yet to see their payments increase will be fixed-rate borrowers who originated their mortgages in 2020 and beyond and they are due to see significant increases to their mortgage interest. If we zoom out though, and look at all homeowners, 39% of respondents simply don’t have a mortgage and as such are not impacted by changing rates. So while a large percentage of borrowers are facing increasing payments in the months and years ahead, they only represent 26% of all homeowners as high interest rates don’t affect everyone equally.

As we move through the balance of 2024 it’s clear that consumers (like analysts) will be keeping a keen eye on the Bank of Canada. Although consumers expect rates to come down over the next year, taking steps towards actually making a purchase may, for many, have to wait—at least until the Bank begins to lower its policy rate. With that in mind we’re eagerly waiting for June 5th, when the Bank makes its next rate decision. We should see a cut—but will it be enough to entice buyers back into the market?